Following on from the trade war between China and the US and the outbreak of the Covid-19 pandemic, the war in Ukraine is the next blow to the world’s economic globalisation. Disrupted supply chains and bottlenecks in primary products can lead to drastic price increases. In sectors that are largely dependent on outsourced products, such as vehicle manufacturing, production lines may even come to a complete standstill at times. Governments and companies are being forced to react to the new circumstances. Last year, the US announced that it would support domestic production of semiconductors, with more than USD 52 billion. Sporting goods manufacturers, such as Nike or Adidas, also need to broaden their production base to reduce dependence on countries such as Vietnam or Indonesia, which have been particularly hard hit by regional lockdowns. Many German companies are also suffering from the effects of the war in Ukraine. Thyssen Krupp, for example, needs nickel for production of its stainless steel, much of which is sourced from Russia. Building up alternative sources of supply requires time but also means higher prices. Reliable supply routes and an improvement in supply security are now on the agenda for many sectors. Higher transport costs, as a result of increased energy prices, mean increased prices, as do higher warehousing costs and lower shares of production in low-wage countries. In a nutshell: this is nothing other than a reversal of globalisation. The consequence of this development is efficiency losses and, as a result, higher consumer prices. Companies that cannot pass on these higher prices to their customers will have to go out of business in the medium term. Wars generally have an inflationary effect. They promote protectionism and increase government spending through unproductive military upgrades. Europe is currently heading in precisely this direction. Lower growth due to efficiency losses, coupled with rising prices and higher military spending, are leading to a loss of prosperity for the people of Europe.

The times of easy money are over

Even investors who benefited from the meteoric success of the large consumer-oriented technology companies in the 2010s are gradually entering shallower waters. Companies like Google, Apple, Facebook, PayPal or Alibaba often represent large holdings in private portfolios. However, the characteristics of these typical Nasdaq stocks have changed radically in recent years. They now account for a large proportion of the gains in global equity indices. However, the likelihood that they will continue their growth trajectory of recent years is becoming increasingly doubtful. It is now clear that these platforms are being hampered by their own size. Or to put it another way: they have reached a dimension that makes marginal utility smaller while costs continue to rise. So, we are talking about negative economies of scale, because the corporation is becoming increasingly more important than the actual product. Both the EU and the Biden administration now agree that monopoly and antitrust issues are no longer just about the financial loss to consumers. Rather, the focus is on the, sometimes insidious, abuse of data and personal rights. In China, for example, the intention to protect consumers and curb gambling addiction in video games is leading to very drastic and immediate regulatory measures. For tech platforms around the world, the increasingly tight regulatory corset is weakening the platform effect on which the current high profitability is based. Increasing numbers of employees in compliance departments, as well as managers who are busy having to defend their companies against government regulation, inhibit the innovative power of corporations that once ensured their ascent. From an investor's perspective, the key question in the coming years will be whether the remaining growth can more than compensate for the decline in valuation levels of these companies. However, despite a significant decline in the pace of growth, it should be noted that increasing regulation raises the barriers to entry for potential competition and naturally protects the continuation of business models.

The FAANG shares of the next 10 years?

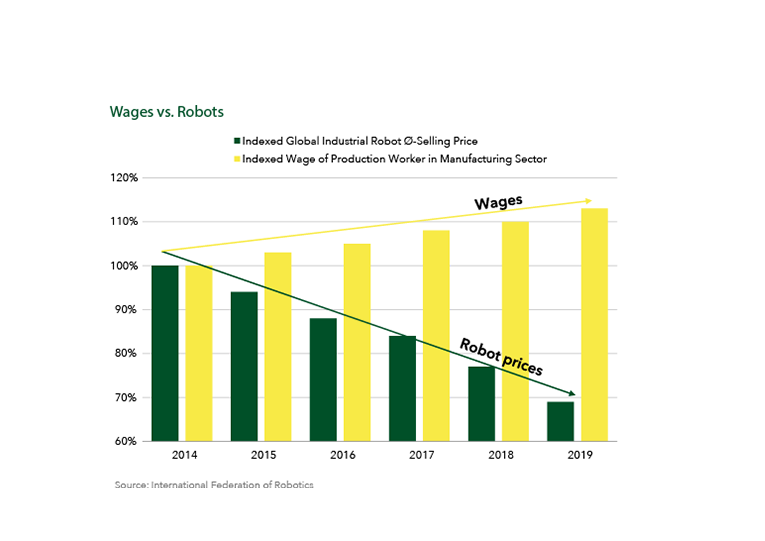

The first phase of the information age began in the 1980s and really took off in the 1990s. It involved the widespread introduction of the personal computer and equipping large companies as well as public authorities and governments with software, digitising information flows and storing data. So-called ERP (Enterprise Resource Planning) systems spread quickly. Companies such as Microsoft, SAP, Cisco, Dell, HP, and IBM were instrumental in this success. In the second phase, which began in the 2000s, the internet became more widespread among consumers. Audio and visual downloads, online shopping, streaming, information dissemination on social networks and the introduction of the smartphone, were the key developments that gave birth to the tech giants of today. They are household names. However, most of the companies from the first phase did not make the leap into this second phase, which continues to this day. Microsoft is one of a few exceptions. Today's so-called tech platforms are sitting on huge profits and have a stable position in the market due to their oligopolies. Facebook and Google dominate the advertising business, Amazon and Alibaba online retail, and Apple and Samsung the smartphone market. But only a few of these currently dominant players will continue to be successful in the third phase of the information age, which is just beginning. The next decade will be the age of digitalisation of production, sustainable energy production, the use of artificial intelligence in various fields, and the electrification of transportation. Components that were once made by human beings will come out of the 3D printer in one piece, and production halls will be scarcely manned by people. Tesla's Gigafactories in Berlin and Shanghai are leading the way. Globally, there are now more than three million industrial robots working day and night, weekdays and weekends. And the trend is growing fast. It is only in the last few years that the available computers have been able to deliver the computing power needed to install self-learning systems and automation solutions in factories. Various industries will increasingly rely on the use of robots, whether for sports shoes or car parts, cosmetics or logistics processes. The Covid-19 pandemic and the further tightening of supply chains due to the Russia-Ukraine war are probably the strongest catalyst for this development imaginable. Companies that, due to supply shortages, are currently setting up production more locally are now facing much higher labour costs. The price of industrial robots, on the other hand, has more than halved in recent years.

Setting targets for a carbon-neutral energy supply has also become increasingly popular in recent years, particularly as a result of the EU's Green Deal. Recently, runaway energy prices and efforts to achieve energy independence from Russia have given additional tailwind to the promotion of renewable energies. The electrification of private mobility is also part of the package of measures, particularly in the EU.

Who will be the winners of this next technological wave? It is all about commodities. Commodities that are necessary for automation, and for generating, storing and consuming green electrical energy. This means semiconductors and the tools to make semiconductors. But real commodities like nickel, copper, lithium are also inevitable in this next phase of technological growth. The production of batteries is primarily about economies of scale. The result will be gigantic battery corporations that will emerge in the next few years. E-vehicle manufacturers that are as vertically integrated as possible and have very few inherited liabilities from the diesel/petrol past to clean up will also benefit. In addition to some automation specialists and computer chip developers, emerging cloud companies will also grow strongly. Artificial intelligence (AI) will become imperative. The companies that manage to make sense of this new technology will gain in importance. The most promising AI application fields are data security, credit analysis, robot production, medicine, genetic analysis, logistics, advertising, energy generation and autonomous driving.

The structural changes require a particularly long-term orientation in terms of capital investment. We take this into account in our funds, the MainFirst Global Equities Fund, the MainFirst Global Equities Unconstrained Fund, the MainFirst Absolute Return Multi Asset and the MainFirst Megatrends Asia, incorporating the investment themes of the car of the future, cloud computing, semiconductors, artificial intelligence and automation.

Author: Jan-Christoph Herbst, Portfolio Manager of the MainFirst Global Equities Fund, MainFirst Global Equities Unconstrained Fund, MainFirst Megatrends Asia and MainFirst Absolute Return Multi Asset

DISCLAIMER

This is a marketing communication.

This marketing communication is for information purposes only and provides the addressee with guidance on our products, concepts and ideas. This does not form the basis for any purchase, sale, hedging, transfer or mortgaging of assets. None of the information contained herein constitutes an offer to buy or sell any financial instrument nor is it based on a consideration of the personal circumstances of the addressee. It is also not the result of an objective or independent analysis. MainFirst makes no express or implied warranty or representation as to the accuracy, completeness, suitability, or marketability of any information provided to the addressee in webinars, podcasts or newsletters. The addressee acknowledges that our products and concepts may be intended for different categories of investors. The criteria are based exclusively on the currently valid sales prospectus. This marketing communication is not intended for a specific group of addressees. Each addressee must therefore inform themselves individually and under their own responsibility about the relevant provisions of the currently valid sales documents, on the basis of which the purchase of shares is exclusively based. Neither the content provided nor our marketing communications constitute binding promises or guarantees of future results. No advisory relationship is established either by reading or listening to the content. All contents are for information purposes only and cannot replace professional and individual investment advice. The addressee has requested the newsletter, has registered for a webinar or podcast, or uses other digital marketing media on their own initiative and at their own risk. The addressee and participant accept that digital marketing formats are technically produced and made available to the participant by an external information provider that has no relationship with MainFirst. Access to and participation in digital marketing formats takes place via internet-based infrastructures. MainFirst accepts no liability for any interruptions, cancellations, disruptions, suspensions, non-fulfilment, or delays related to the provision of the digital marketing formats. The participant acknowledges and accepts that when participating in digital marketing formats, personal data can be viewed, recorded, and transmitted by the information provider. MainFirst is not liable for any breaches of data protection obligations by the information provider. Digital marketing formats may only be accessed and visited in countries in which their distribution and access is permitted by law.

For detailed information on the opportunities and risks associated with our products, please refer to the current sales prospectus. The statutory sales documents (sales prospectus, key investor information documents (KIIDs), semi-annual and annual reports), which provide detailed information on the purchase of units and the associated risks, form the sole authoritative and binding basis for the purchase of units. The aforementioned sales documents in German (as well as in unofficial translations in other languages) can be found at www.mainfirst.com and are available free of charge from the investment company MainFirst Affiliated Fund Managers S.A. and the custodian bank, as well as from the respective national paying or information agents and from the representative in Switzerland. These are:

Austria: Raiffeisen Bank International, Am Stadtpark 9, A-1030 Wien, Österreich; Belgium: ABN AMRO, Kortijksesteenweg 302, 9000 Gent, Belgium; Finland: Skandinaviska Enskilda Banken P.O. Box 630, FI-00101 Helsinki, Finland; France: Société Générale Securities Services, Société anonyme, 29 boulevard Haussmann, 75009 Paris, France; Germany: MainFirst Affiliated Fund Managers (Deutschland) GmbH, Kennedyallee 76, D-60596 Frankfurt am Main, Deutschland; Italy: Allfunds Bank Milan, Via Bocchetto, 6, 20123 Milano MI, Italy; Lichtenstein: Bendura Bank AG, Schaaner Strasse 27, 9487 Gamprin-Bendern, Lichtenstein; Luxembourg: DZ PRIVATBANK S.A., 4, rue Thomas Edison | L-1445 Strassen; Portugal: BEST - Banco Eletronico de Servico Toal S.A., Praca Marques de Pombal, 3A,3,Lisbon; Spain: Societe Generale Sucursal en Espana, Calle Cardenal Marcelo Spinola 8. 4t planta. 28016 Madrid, Spain; Sweden: MFEX Mutual Funds Exchange AB, Grev Turegatan 19, Box 5378, SE-102 49, Stockholm, Sweden; Switzerland: UBS Fund Management AG, Aeschenplatz 6, 4052 Basel, Switzerland; UK: Société Générale Securities Services, Société Anonyme (UK Branch), 5 Devonshire Square, Cutlers Gardens, London EC2M 4TL, United Kingdom

The investment company may terminate existing distribution agreements with third parties or withdraw distribution licences for strategic or statutory reasons, subject to compliance with any deadlines. Investors can obtain information about their rights from the website www.mainfirst.com and from the sales prospectus. The information is available in both German and English, as well as in other languages in individual cases. Explicit reference is made to the detailed risk descriptions in the sales prospectus.

This publication is subject to copyright, trademark and intellectual property rights. Any reproduction, distribution, provision for downloading or online accessibility, inclusion in other websites, or publication in whole or in part, in modified or unmodified form, is only permitted with the prior written consent of MainFirst.

Copyright © 2022 MainFirst Group (consisting of companies belonging to MainFirst Holding AG, herin „MainFirst“). All rights reserved.