Innovation has always been one of the main drivers of economic growth and a mainstay of future development. 2022 has brought a series of unforeseen events and developments around the world.

The war in Europe, as a humanitarian crisis, is not only causing fear and dread but is also precipitating the transition to renewable energy (especially in Europe). Despite ongoing supply shortages, the semiconductor industry is increasingly gaining in importance, in addition to political conflicts of interests, it also holds substantial potential for development. In the current uncertain markets in particular, innovative companies can establish themselves as new value drivers and bring about a fundamental structural change in their sectors.

On the one hand, the economic and political environment is currently being shaped by rapid and decisive changes while, on the other, innovation-oriented investment strategies continue to come to the fore.

Renewable energies

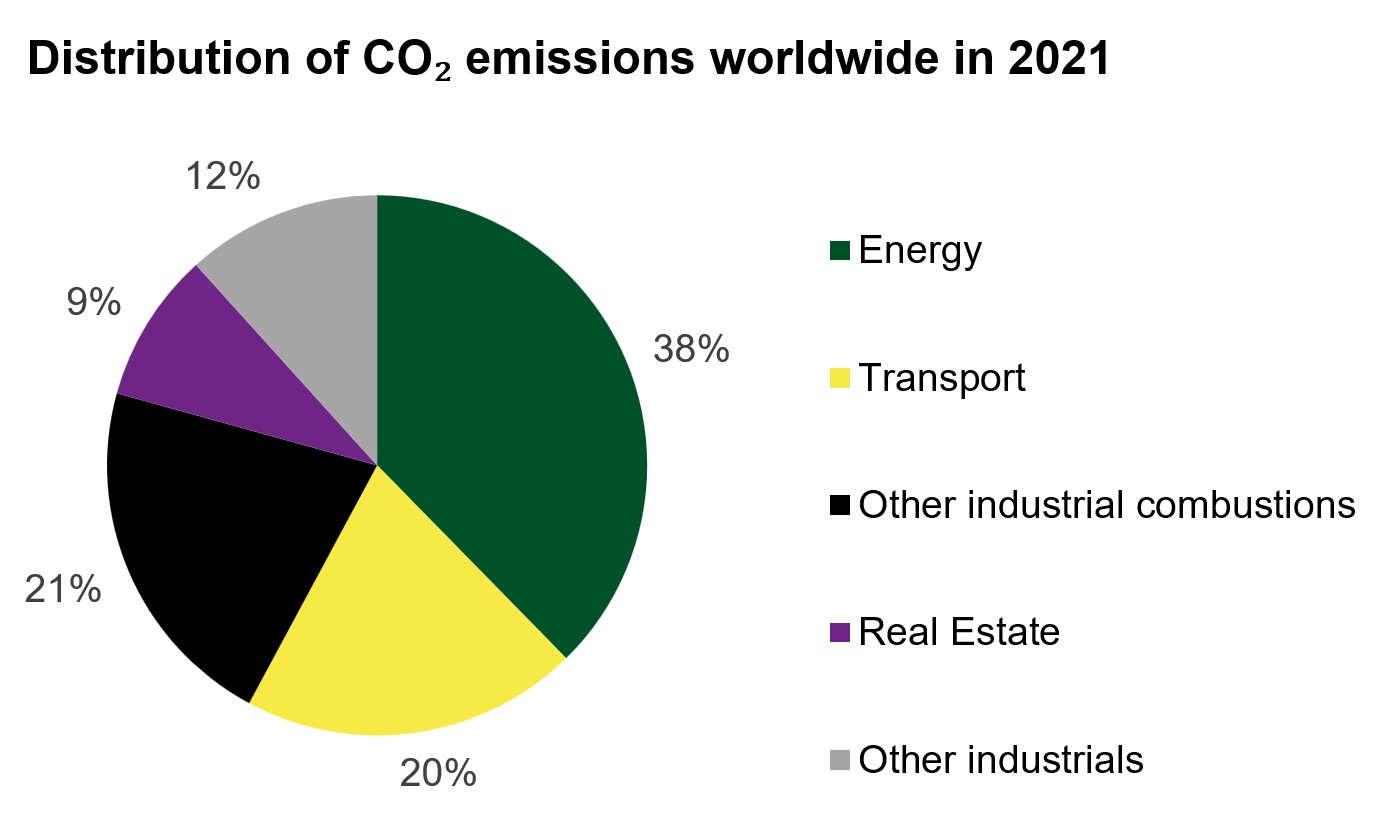

The energy sector still accounts for the biggest percentage of global carbon emissions, totalling 38 %, which is why innovations in this sector are interesting and make sense both from an ecological and an economic perspective.

Graphic 1 / Source: EDGAR/JCR, Crippa, M. et al, Statista, As of 2021

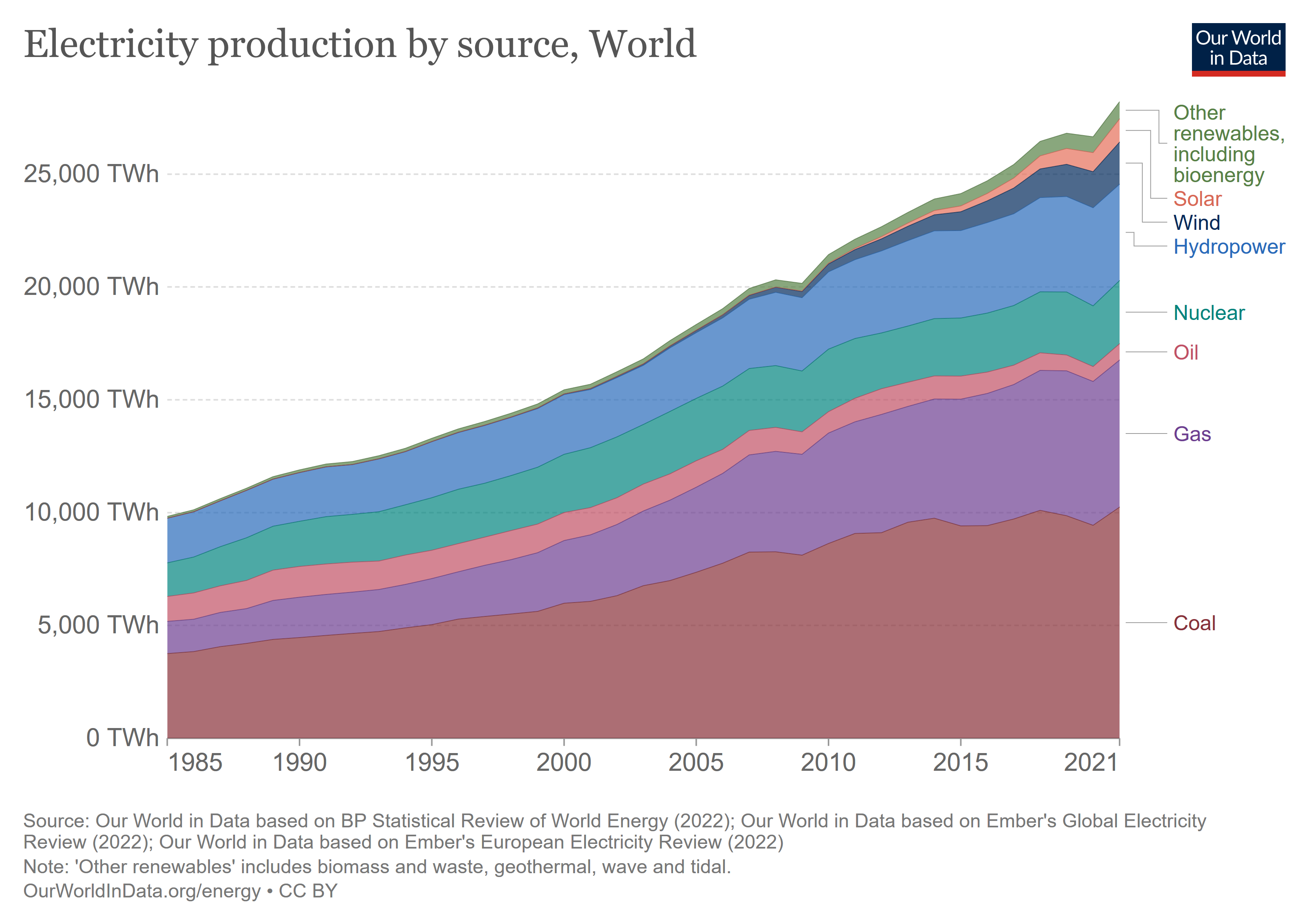

At the current state of the art, renewable energies are one of the biggest prospects, as they hold potential to win a steadily growing share of the energy market and for high levels of investment and profits. Like the Fukushima nuclear disaster and the Libyan Civil War in 2011, Russia’s war in Ukraine marks a crucial turning point for the worldwide energy sector, but especially for Europe’s energy policy. Similar to what happened in 2011, we expect the global expansion of liquefied natural gas to accelerate as global short-cycle oil production and global fungible gas reserves revive.

Graphic 2 / Source: https://ourworldindata.org/energy (Hannah Ritchie, Max Roser and Pablo Rosado (2022))

However, we are also seeing some differences. In 2011, the sector was in a seven-year cycle of exploration and development of megaprojects, which were driving the expansion of resources and the revival of growth outside the OPEC. The current situation is just the opposite. After seven years of too little investment in hydrocarbons (2015-21), shrinking oil reserves (-50% since 2014) and the smaller proportion of shale gas coming from non-OPEC countries, significantly greater capital spending is needed for short- and long-term projects. Also, the ongoing focus on decarbonisation, which also entails higher capital costs when developing oil and gas fields, means that this energy investment cycle will be different and is characterised by the growing importance of renewable energies.

Transportation and batteries

The decarbonisation process is evolving from a one-dimensional to a multi-dimensional ecosystem as capital markets, companies and governments are expanding their sustainability efforts and focus on a broader spectrum of clean technologies. Four technologies have emerged as transformative and are playing a leading role in the pathway towards carbon neutrality, specifically renewable energies, clean hydrogen, carbon sequestration and battery storage.

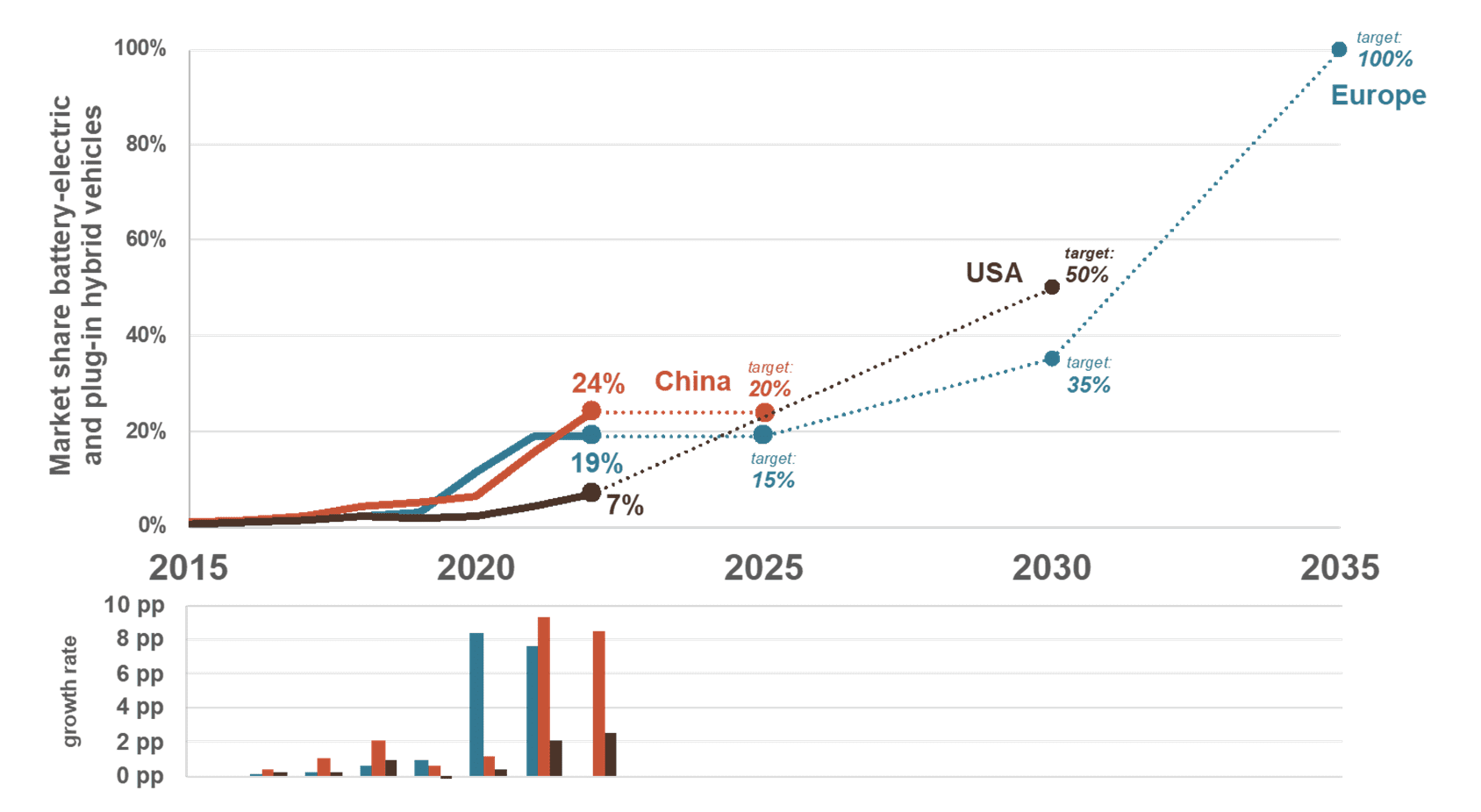

As Fig. 1 shows, transportation is the second-biggest carbon-emitter, and innovations are underway in this sector too. Electric and hybrid vehicles are gaining more and more market share and are receiving political support due to their importance in climate change.

Graphic 3: Historical development of the market share of all-electric and plug-in hybrid vehicle models in all new registrations as well as future targets for China, Europe and the United States / Source: https://theicct.org/2022-update-ev-sales-us-eu-ch-aug22/

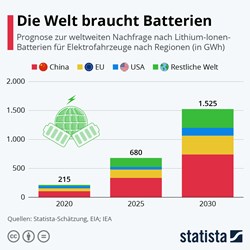

Therefore, batteries and the raw materials required for them, will become increasingly more important in the future. Lithium batteries are very common at the moment and thus require large quantities of lithium. From extraction of raw materials to the point where the battery is in the car, the entire value chain is important for investors. In addition to the transport sector, batteries are also gaining in importance in the energy sector, due to the expansion of renewable energies. Most notably in wind and solar energy, where the possibility of energy storage would be a game-changer.

The automotive industry is on the verge of a major turning point, with vehicles that are increasingly connected and software-defined, including electric and autonomous vehicles. If car manufacturers succeed in marketing the new value of these vehicles (e.g. fuel savings, safety and pleasure in driving), they should be able to generate profits beyond the limits of their current business models. Industry realignment could become a key theme for EV batteries and vehicle OS (operating systems). We consider companies with scalable products (e.g. shared architecture for EVs) to be in a better position at present than automotive manufactures that offer a broad range of models and drivetrains.

In the development of electric vehicles, the main shift in research took place in the drivetrain area (20% to 30% of added value). However, autonomous cars will change added value in all areas of vehicle development. The shift from engines to batteries has facilitated consolidation within the battery industry as well as the formation of battery-only companies.

Graphic 4: "The world needs batteries" - Forecast for global demand for lithium-ion batteries for electric vehicles by region (in GWh) / Source: https://de.statista.com/infografik/25389

Semiconductors

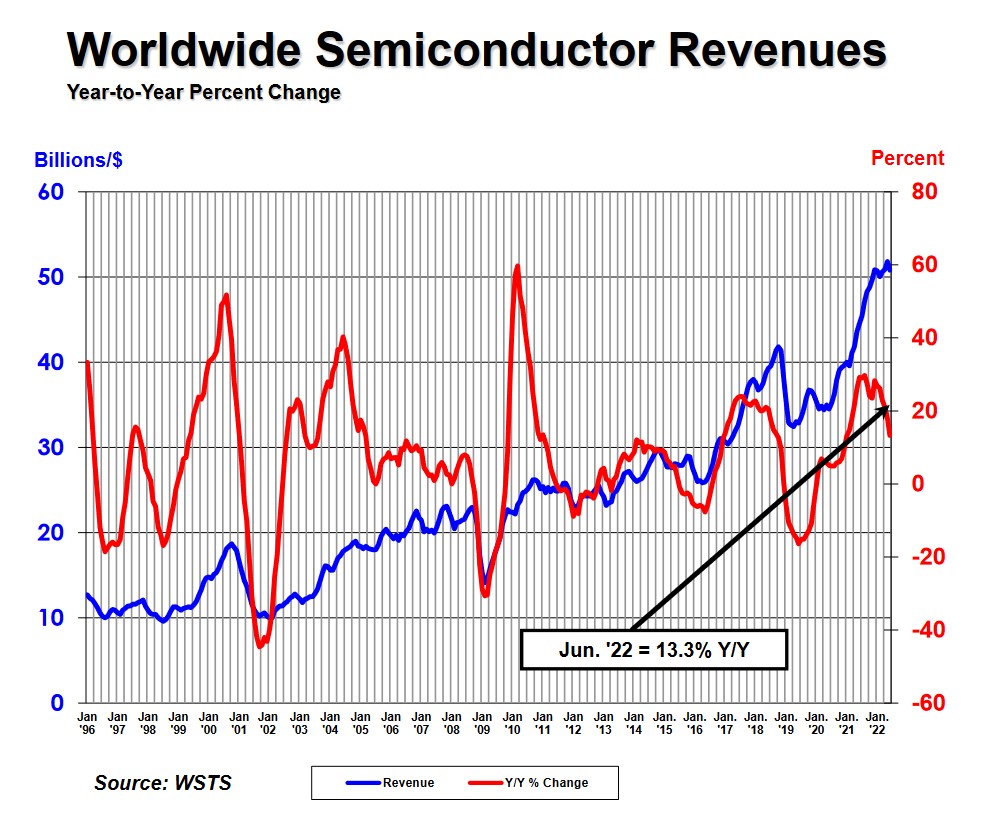

Processors are now a cornerstone of the global economy and, although computers, mobile telephones and servers are no longer the only devices they are found in, their political and economic importance is increasing. Asia currently produces 75% to 80% of global chips; mainly in Taiwan, South Korea, China and Japan. At the moment, 92% of processors with transistors smaller than 10 nm are exclusively produced by TSMC in Taiwan. Samsung in South Korea holds the remaining 8 percent of production of these processors. This puts Taiwan in a place of political prominence, while the company TSMC is more to the economic fore. The spotlight is also on the company ASML, which, as a manufacturer of semiconductor production equipment and a supplier of TSMC, occupies a similar monopolistic position in the market. The innovative semiconductor market holds considerable growth potential along the entire value chain, thanks to its growing technological and thus economic importance. Despite the recent macro and geopolitical changes, which have led to a short-term decline in demand, long-term growth of the semiconductor industry remains intact thanks to the increasing quantity of silicon used in end devices.

Graphic 5 / Source: https://www.semiconductors.org/global-semiconductor-sales-increase-13-3-in-q2-2022-compared-to-q2-2021/

Digital transformation

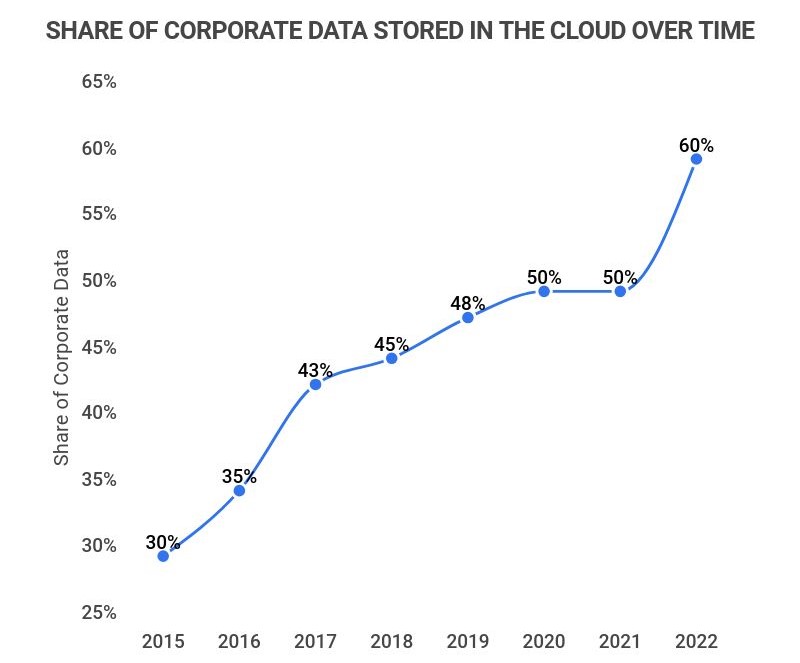

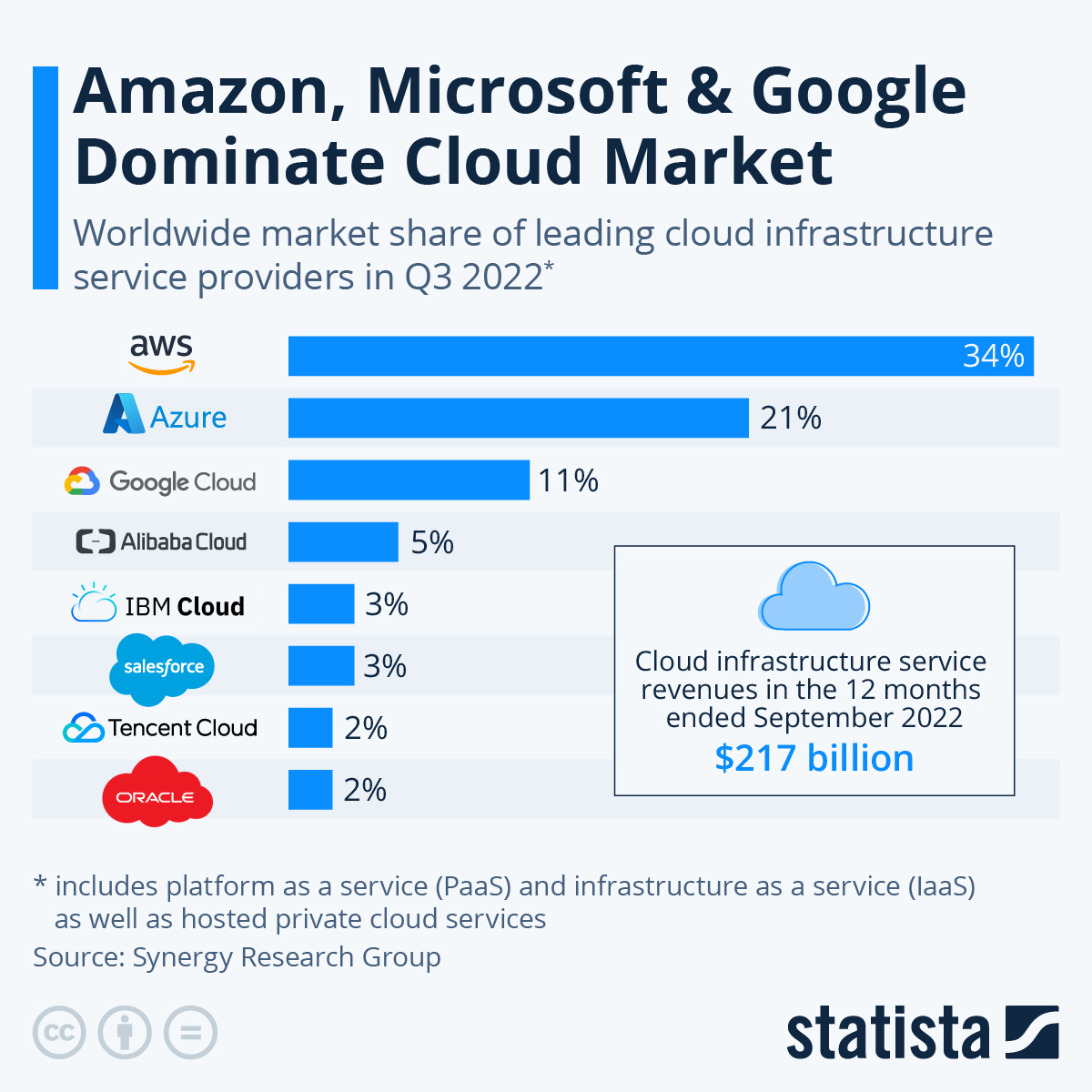

The digital transformation is driving new software segments worth billions and the outsourcing of capacities to large server farms as data centres is one of the logical next steps in the optimisation of digital data processing.

Graphic 6 / Source: https://www.zippia.com/advice/cloud-adoption-statistics/

Graphic 7 / Source: https://www.statista.com/chart/18819/worldwide-market-share-of-leading-cloud-infrastructure-service-providers/

Activities and processes in the digital age require enormous computing power and, above all, generate huge amounts of data. These digital business processes also require common data models that must provide a 360-degree view of the digital infrastructure of a customer, an employee, a patient, a design, a building, a bridge, a machine, etc. These models generate scalable sets of data, which can be used, for example, by artificial intelligence. This will probably convey an unbeatable competitive advantage and secure market position for industry leaders.

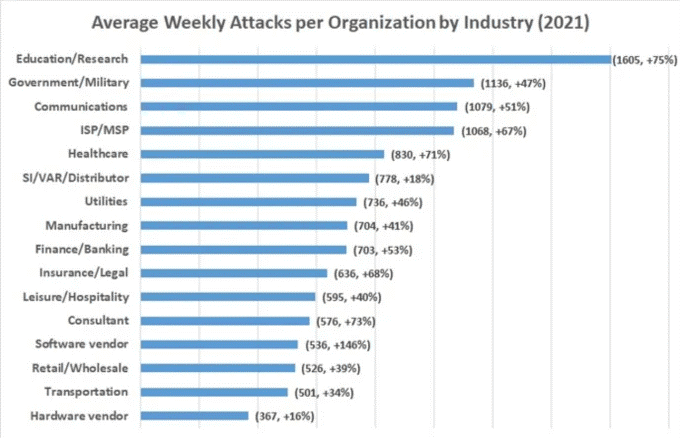

Whether machine-learning programs or artificial intelligence (AI), new software solutions will be needed to process the large volumes of data as efficiently and quickly as possible. And ideally also securely, which is why the whole area of cybersecurity is one of the up-and-coming segments in the 2020s and, as it undergoes constant development, continually embraces new challenges in information processing. The value of speed in AI and machine learning has the potential to drive the trend towards cheaper hardware in the construction of data centres and networks. This could lead to substantial shifts in the breakdown of spending on hardware, software and services. AI and machine learning (ML) can drive productivity gains, which will benefit economic growth, profitability, return on investment and the valuations of assets.

Graphic 8 / Source: https://www.pcquest.com/cyber-security-awareness-month-40-increase-weekly-cyber-attacks-organizations-worldwide-2021/

Conclusion

Innovation is essential in all areas of life and the economy – for progress, change and to introduce new technologies and opportunities. It’s what paves the way into the unknown and it’s the reason for the euphoria at each new discovery – including in the capital markets. For decades, the MainFirst Global Equities team has focused on just such discoveries, meticulously tracking technological developments and advancements across all sectors to achieve long-term growth through targeted investments in the most disruptive business models, driving our world and economy.