The 2020s have thrown up many challenges for the global markets so far. After a pandemic lasting almost three years and loose monetary policy, the Russian invasion of Ukraine sent the world into another unforeseen spin. The economic implications, rising energy costs and climbing inflation forced central banks to take drastic steps in the form of interest rate hikes. Europe was hit particularly hard by these new challenges, and it and the US faced key rates we hadn’t seen for almost two decades.

2023 passed with a slight let-up in equity markets. Despite the averted banking crisis in the first half of the year, ongoing high interest rates and the emergence of further geopolitical conflicts, most equity markets surprisingly managed to close in positive territory. This astounding resilience amid the ongoing certainty paints a fascinating picture of the ability of the financial markets to bounce back.

Even with various global crises underway, European markets grew by a remarkable figure of almost 30% between the start of 2020 and the end of 2023¹. But closer analysis of this period reveals that small and mid-cap equities lagged well behind the blue chips. This trend raises interesting questions about the underlying dynamics and strategic decisions. All the same, we shouldn’t lose sight of the outstanding performance of large caps. These companies form the backbone of popular index funds and their names are familiar to people who have nothing to do with professional investment analysis. In uncertain times, large caps ostensibly offer stability. The logical consequence is that many investors allocate a large chunk of their portfolio to large caps. Such companies not only package themselves as financial instruments but also as pillars of solidity amid the turbulence of the markets.

However, anyone who invests only in blue chips is missing out on a major opportunity as, historically, small and mid caps have always outperformed large and established companies over the long term. Anyone who invested in European small caps 20 years ago has locked in a total return of 495%, compared with only 226% for European large caps.²

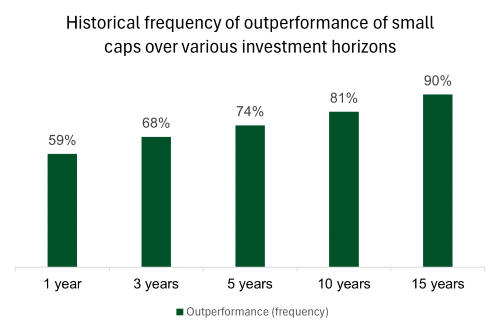

Clear trend: second-tier stocks are clear outperformers in the long run

An analysis of the MSCI from November 1975 to June 2023 shows that this is not a one-off and that second-tier stocks outperform blue chips over longer horizons outside of Europe as well. It turns out that nine times out of ten in the past, small caps have outperformed large caps over a 15-year investment horizon.

The chart shows the percentage of cases in which small cap stocks (MSCI World Small Cap Index) outperformed large cap stocks (MSCI World Index) in a rolling-window analysis. The period of analysis is from November 1975 to June 2023. For data availability reasons, the MSCI World Equal Weighted Index was substituted for the MSCI World Small Cap Index track record prior to December 1998.³

One reason for this is that small and mid-sized companies not only have more scope for growth but can also be more flexible and innovative. These companies often have less red tape, which enables them not only to act more quickly but to react to changes with agility. This inherent agility is a key advantage.

In an ideal scenario, it is worth investing in second-tier stocks if the company starts out as a small or medium-sized company and grows into a market leader. During this process, the investor’s shares continually go up in value, undoubtedly a gratifying development. Of course, not all small and mid-sized companies make it to the top. The road is littered with obstacles and many companies fall by the wayside. That said, investment in second-tier stocks remains attractive, since they offer a unique opportunity to participate in dynamic developments and potentially achieve outstanding returns.

In MainFirst Top European Ideas and Germany Fund, we are unrelenting in our search for these gems. In selecting our companies, we prioritise not only operational and financial strength but in particular also the calibre of management. We focus on family-run enterprises and on managers who think and act like entrepreneurs. Concentrating on these aspects enables us to select companies which are not only successful in the short term but also have long-term growth potential.

We also place emphasis on evaluating the companies and their structural growth potential. We as a team hold up to 300 meetings with the management teams of our portfolio companies or potential candidates. When we identify promising candidates for our portfolio, we invest long-term and hold onto high-quality companies even in tough markets rather than rushing to sell them.

The past three years have been challenging for second-tier stocks, since investors often tend to fall back on the supposed safe havens in uncertain times. The higher key rates have also made bonds and money market funds more attractive, prompting many investors to take their money out of the equity markets. Despite these challenges, we are firm in our conviction that the careful selection of companies and long-term investment will bring about lasting success.

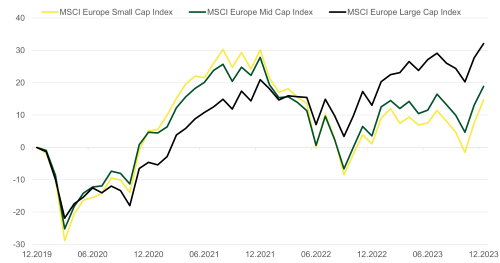

Unusual situation: blue chips have outperformed secondary stocks by a clear margin since 2020.

In absolute and relative terms, European second-tier stocks seem to be more undervalued than they have been in a long time. While the major leading indices such as the MSCI Europe, the STOXX 50 and the DAX had already or very nearly reached new heights at the end of 2023, the small cap indices are still well below their record-highs of recent years. This presents investors with attractive return opportunities.

We are amazed that the discounts at which second-tier stocks are trading to blue chips have hardly come down at all over the past year. Incidentally, this is a global phenomenon, with the trend in valuations in recent years going from a P/E ratio premium for secondary stocks to a discount.

On 14 December, Federal Reserve Chair Jerome Powell, signalled the possibility of the end of the rate hike cycle and the start of rate cuts in 2024 but did not go into detail. Immediately afterwards the SDAX rose by an impressive 3.5%, while the DAX actually fell by a marginal 0.1%. The MSCI Europe Small Cap Index also rose by a substantial 3.2%, far more than the MSCI Europe Large Cap Index, which only gained 0.5%. We saw the market react in a similar fashion one month prior, on 14 November, when a marked slowdown in US inflation was reported and markets interpreted this as the first sign that interest rate cuts were on the way. This emphatically highlights the long-term potential that second-tier stocks harbour.

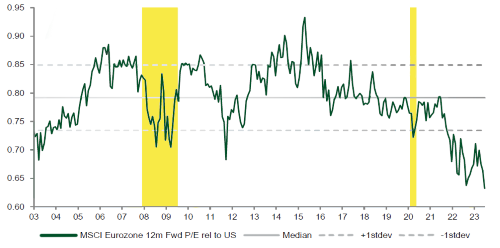

In addition, European stocks are trading at a substantial discount to US stocks. This difference in valuations not only illustrates the differing market conditions but also presents a promising opportunity for observant investors. While American markets sometimes trade at higher valuations, European second-tier stocks seem to be undervalued, which creates upside potential and scope for attractive returns. This dynamic illustrates that the reactions to monetary announcements and economic signals not only cause short-term shifts in markets but can also open up long-term opportunities for smart investors.

European equities are trading at a relatively high discount to US stocks.⁴

The discerning investor sees the relative attractiveness of second-tier stocks versus large caps. Either large-cap stocks are currently overvalued or else small-cap stocks are undervalued. This subtle balance provides scope for strategic thinking and tactical decisions in the portfolio.

The same deductive approach also applies to European versus US equity markets. An investor who buys the right securities at this time theoretically stands to benefit if the valuations of small and mid caps versus large caps and the valuation of European equity markets relative to the American equity markets return to their historical average. This creates an opportunity for potential performance that is not just limited to short-term fluctuations but holds out the long-term prospect of optimising returns.

So, if you wish to participate in stock market gains in the coming decades, it could prove advantageous to invest in funds that focus on small and mid cap equities. These companies not only have the potential to grow and innovate but also reflect the diversity and resilience of the broader market. The art of investment is not only about finding short-term opportunities but also about being foresighted, in order to benefit long-term from the macro- and micro-economy.

¹ Figure 1. MSCI EUROPE TR from 31 December 2019 to 31 December 2023. Source: Bloomberg.

² Figure 2. MSCI EUROPE Large Cap TR and MSCI Europe Small Caps from 31 December 2003 to 31 December 2023. Source: Bloomberg.

³ Source: MSCI “Small Caps Have Been a Big Story After Recessions”

⁴ Source: JP Morgan Nov. 2023