Subdued mood

After an exceptionally weak 2022, the majority of investors seem to harbour a health sense of scepticism about growth stocks. Some people are even comparing the current situation to the dot-com bubble around 20 years ago. Many companies that were complaining about a shortage of IT specialists at the start of the pandemic are now making job cuts. For example, many of the tech platforms have announced layoffs, including 10,000 at Microsoft, 12,000 at Alphabet and 18,000 at Amazon. Considering that these three companies generated record-breaking revenues in 2022, these measures can be interpreted as a signal of a weaker environment to come. But are the current growth prospects really that dire or are we currently seeing the perfect example of a pork cycle that holds great opportunities for investors right now? To be able to form an opinion, we first need to place the situation in the historical context.

What we have experienced since the beginning of the pandemic is likely to be discussed in business circles for many years yet. How did the individual business models cope with the challenges of lockdowns and supply chain issues? What processes are required for the future to be better able to deal with such crises? In the immediate aftermath, however, some sectors seem to be suffering a sort of hangover. For instance, PC manufacturers are reporting double-digit declines in revenues after the boom of 2020/2021. Market leader Lenovo, for example, turned over 24% less in the fourth quarter. Various semiconductor companies are also reporting declines in revenues of late, as the supply shortages of recent years seem to be resolved and thus the price of an 8Gb standard DRAM chip (Bloomberg ISPPDR37 Index), at USD 1.80, is around 50% below the previous year’s level.

It’s important to note, however, that the price competition has intensified, especially in relation to memory chips for consumer electronics (smartphones, laptops, etc.). The mood at companies such as Samsung, SK Hynix and Micron Electronic is therefore subdued. Intel even reported a net loss last quarter. Unsurprisingly, companies are announcing cuts in planned investments – a basic requirement for stabilising the supply and demand situation.

Graphic 1: Memory chip sector - stock performance correlates with year-on-year price changes. Source: Morgan Stanley Research, as at 17 January 2023

In contrast, there still seem to be substantial delivery times for semiconductor solutions for the automotive industry. This reflects the growing demand for electric vehicles, which require much more semiconductors in direct comparison with combustion-engine vehicles, e.g. MOSFETs for battery management. For them, the situation is far from dire.

A new era

Within the microprocessor subsegment, however, the ongoing positive sentiment of companies involved in the production of high-performance semiconductors is obvious. Only recently the incentives brought in under the US CHIPS and Science Act to fund domestic production of microprocessors led to a spate of announcements in investment in new chip facilities. Companies with the necessary equipment to manufacture the most advanced chips are experiencing an unrelenting boom in orders. In particular, the EUV machines of Dutch firm ASML, which are capable of manufacturing chips smaller than 10 nm, are booked out for years. ASML’s order book is currently worth EUR 60 billion.

However, there are countless examples of investments made for purely protectionist reasons not creating sustainable value. This raises the question whether the necessary demand exists for the chips funded under the CHIPS and Science Act and whether the planned investments will actually cover the capital costs. From the point of view of economic policy, it should be less about just creating jobs in a growth sector, and more about reducing dependency on Asian suppliers.

The fund management of MainFirst’s Global Equity strategy expects that technology development is again entering a new era – regardless of political funding. According to it, artificial intelligence should trigger the next quantum leap in terms of the digitalisation megatrend. This theory is being backed up right now by the number users signing up to ChatGPT. If AI-based chatbots with their self-learning algorithms become standard, a staggering amount of computing power will be required. Demand for high-performance processors could therefore be looking up.

The race to supply for supercomputers

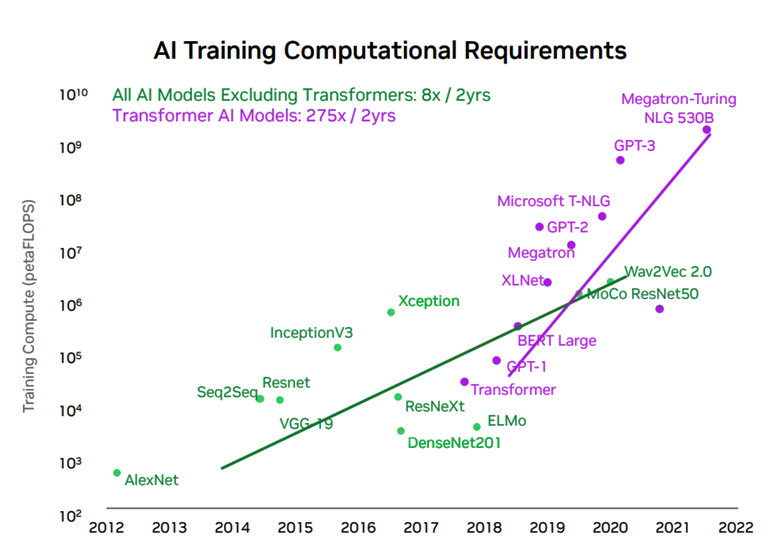

For AI-based learning models, graphics processing units (GPUs) provide the necessary computing power, as they are specially designed to do multiple computations in parallel. The clear market leader in GPUs recognised early the exponential growth of computing power entailed in self-learning applications and positioned itself with dedicated product solutions. According to Top500.org, Nvidia supplies the processors for 361 of the 500 most powerful supercomputers in the world. The evolution of the areas of application from traditional machine learning through deep learning and on to inference (making predictions from a trained model) requires more and more parameters to be processed in a model at the same time. The latest freely available version of ChatGPT, GPT-3, requires more than 1,000 times the hardware performance capacity compared with the first version in 2018. Normally, computing rate is measured in petaflops, which corresponds to one quadrillion (10^15) floating point operations per second.

Graphic 3: Computational requirements for training transformers - Transfomer AI models require 275x more computing power every two years. Source: Nvidia

Chatbots – just a lot of hype or a permanent revolution?

There is much discussion at present about the benefits and potential dangers of the mass use of natural language processing models like ChatGPT. From a technological point of view, text-based bots are likely to be one of the first areas of application of artificial intelligence, which promises to benefit the general public and is widely accepted. However, the potential implications for society are not without controversy. Analysts have started to mention the potential of chatbots of the future to replace entire fields within the labour market. For example, the Daily Mirror newspaper, founded in 1920, is examining the extent to which its employees can use chatbots to write news in brief and thus automate traditional journalism.

To show how far-reaching the changes that machine learning models could bring about are, let’s look at the Internet search. To date, searches for certain search terms were done by algorithms, which referred to the contents of certain websites. For example, if you did a search for a legal matter, you would get a link to a piece of legislation or a link to commentaries about this piece of legislation. In contrast, an AI-based bot could provide you with the correct basis for the claim as well as a legal interpretation of the matter. In addition, users can follow up on the answers provided, and refine the results by interacting with the bot. Chatbots could thus act as a sort of assistant for various searches without us having to do the research ourselves. Increasing productivity with the aid of chatbots seems possible in many areas of work.

It is no surprise that the signups to Open.AI, the operator of ChatGPT, have shot up and, of late, registrations have even surpassed those of the previously most successful app, TikTok. Although the tool was primarily designed for text-based questions, millions of users are now putting the capabilities of AI to the test. Schoolchildren are getting ChatGPT to do their homework and there are even cases of students having ChatGPT write the bulk of their bachelor thesis.

But who is benefiting from this development? It is not yet clear how chatbots will be monetised, as Open.AI Inc. was founded as a non-profit organisation. One of the initial investors was Elon Musk, who was promoting free collaboration with the public and making the results of research available on an open-source basis. However, Microsoft has recently announced an investment of USD 10 billion and is likely to expect a payback.

Microsoft’s investment effectively marks the start of the battle for supremacy in Natural Language Processing. It didn’t take long for the usual players who have AI operations such as Alphabet to launch their own version of a chatbot. In the case of Google’s parent company, its dominant position in the search engine business was also at stake. If Microsoft succeeds in integrating ChatGPT into its search engine BING, some of Google’s lucrative advertising revenue would be in jeopardy. However, Google’s answer, Bard, initially fell short of the high expectations when its skills were presented. Asian companies did not waste any time unveiling their AI bots either. Baidu attracted the attention of the world of technology with its presentation in March of Wenxin Yiyan, called ERNIE bot in English. Further AI tools are likely to follow from JD.com, Netease and Tencent. It remains to be seen which companies will win the global race. However, Microsoft has the significant advantage of being early to market with a solution and, as a large digital platform, being able to complete a complementary integration in existing products.

Incidentally, if you ask ChatGPT who the beneficiaries of the increasing use of chatbots are, you get the following answer:

Widespread use of ChatGPT would likely be beneficial to many companies in a variety of industries. Here are some examples:

- Companies that develop and offer chatbot solutions could benefit from wider adoption and use of ChatGPT, as they can integrate this technology into their products.

- Semiconductor and process manufacturers such as Nvidia and Advantest, which are able to provide the necessary processing power for AI-based applications, could also benefit from a wider use of ChatGPT.

- Cloud computing companies such as Amazon Web Services, Google Cloud and Microsoft Azure, which can serve as platforms for the deployment of chatbot solutions, could also benefit from higher demand for these applications.

- Companies specialising in artificial intelligence and machine learning could benefit from a wider use of ChatGPT, as they could integrate this technology into their own products and services.

- Finally, companies that use chatbot solutions to interact with their customers could benefit from a wider use of ChatGPT, as they would be able to create more effective and comprehensive customer experiences.

10 years of GE – Generating success from the trends in technology

There seem therefore to be many opportunities for companies to benefit from the new possibilities of artificial intelligence. However, firstly, the necessary computing power must be provided for chatbots. A further increase in IT spending appears essential. The announcements made by Alphabet, Microsoft and the Chinese technology platforms alone should amount to double-digit billions of US dollars in investment in IT infrastructure. Data centre operators, too, are pleased with current developments because data volumes are likely to grow exponentially with the increasing use of artificial intelligence. On the other hand, data security and copyright issues are likely to become increasingly important. Everything up to the disruption of existing business models is possible.

From a technological point of view, a period of radical change is looming, which is likely to bring with it certain opportunities, but also risks, for investors. The Global Equities team under Frank Schwarz has many years of experience in dealing with such changes in the technology sector. The added value that the MainFirst Global Equities Fund has been generating for ten years now, and again as at 1 March, for its investors testifies to this. Early investment in digitalisation investment themes, such as cloud computing, cyber security and semiconductor supply, has been contributing to the success of the fund for many years. Now that we have entered the era of artificial intelligence, active portfolio management in the technology sector seems imperative. Frank Schwarz and his team have already set the necessary course for the next ten years.