2022 was one of the toughest years in recent decades for Europe. Russia’s invasion of Ukraine led to what was probably the greatest war in Europe since the end of World War II and an ever-increasing number of refugees. The effects of the war on the continent were an explosion in energy costs – in turn leading to a sharp rise in inflation – and concerns that gas supplies would run out by winter. Central banks responded to the inflationary shock by dramatically hiking rates, and thus put capital markets worldwide under pressure.

The European equity market hit rock bottom in September, at which point many investors had already written off European companies. To the surprise of many, however, the European policy – and Germany’s in particular – proved to be very pragmatic. The federal government put in place many support packages and secured energy and gas supplies. Thanks to these measures, the worst-case scenario was averted.

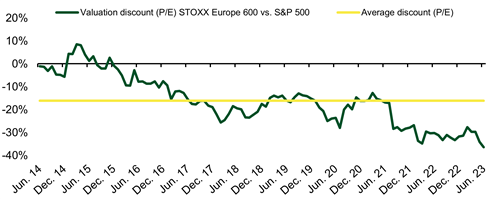

To the delight of investors who did not let the panic get to them or who even bought shares, the markets made a phenomenal comeback. The STOXX Europe 600 TR gained more than 23% between the low at the end of September and the end of June, and thus outperformed its US counterpart, the S&P 500, by a wide margin, which gained less than 11% in the same period. This is remarkable in that the US, being the leading stock exchange location, is regarded as highly dynamic, not just in the recent past but also in historical terms. Despite what feels like constant crises, Europe caught up with and even beat the US in some sectors. Even so, the valuation discount of European equities to US equities actually increased. Thus, the European equity market offers substantial catch-up potential compared with the US.

In recent years, the P/E discount of the STOXX Europe 600 has risen vs the S&P 500

Source: Bloomberg, as at 30 June 2023

2022 was a disappointing year for MainFirst Top European Ideas Fund as well. Many of our equities were caught up in the panic selling. However, many were wrongly punished.

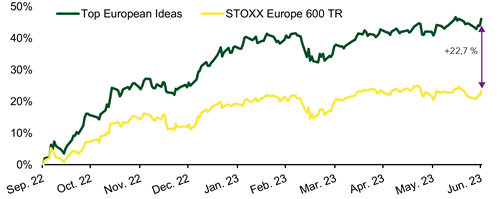

It stands to us in these times that, as early as the company selection stage, we set great store by the calibre of company and management. Good business leaders, especially in times of crisis, are better able to adapt the companies to the environment and to take opportunities that arise. Rather than letting the panic get to us, we continue to trust in our strong companies. Specifically, MainFirst Top European Ideas Fund gained 46% since the end of September 2022, which corresponds to an outperformance of almost 23% over its benchmark.

MainFirst Top European Ideas Fund vs STOXX Europe 600 TR from its low on 29 September 2022 to 30 June 2023

Source: Bloomberg, as at 30 June 2023

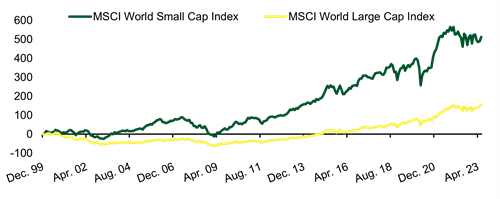

In times of stock market turbulence in particular, investors often tend to flee to the supposed safety of large caps. Second-tier stocks thus underperformed blue chips. This trend is also continuing this year. Investors who are not in on this could therefore miss a real opportunity. Historically, small caps have always outperformed blue chips over longer periods, and this outperformance was generally particularly pronounced in rising markets.

Since most small caps are younger companies, they often have the potential for high growth rates. In addition, they are often concentrated in promising segments or highly profitable niches. Furthermore, they are more flexible and more innovative, their speed of innovation is faster and, above all, they are more entreprising than established concerns, which are often bureaucratic and cumbersome.

Globally, too, small and mid caps outperform by a clear margin

Source: Bloomberg, as at 30 June 2023, currency: EUR

Since analysts and institutional investors generally do not pay as much attention to second-tier stocks as large caps, there are lots of undiscovered gems for observant investors to find.

On the other hand, the large caps can see small caps as potential takeover candidates. These are then swallowed up by large corporations with a high takeover premium.

For investors who are prepared to think long-term and take advantage of the growth potential of smaller companies, the current environment thus offers interesting opportunities.

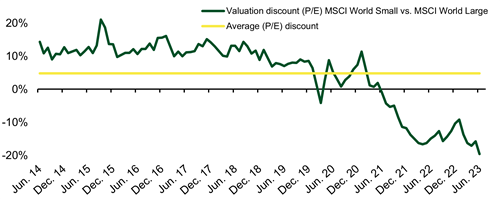

In addition, we have observed that second-tier stocks worldwide are trading at ever higher discounts to standard stocks. This is mainly down to the concerns over economic and political developments in the world. As mentioned, however, we do not share these concerns and see huge catch-up potential in this area too.

Bargain second-tier stocks: comparison of the valuation discount (P/E) between MSCI World Small vs MSCI World Large

Source: Bloomberg; as at: 30 June 2023

Despite our fund’s very good performance to date, we still see plenty more potential for European equity markets, as this economic downturn is already largely priced into share prices. We should never forget that the stock market anticipates future developments.

Plus, not only have most commodities come back down to pre-war levels but electricity and gas prices are also returning to normal. Consequently, inflation is gradually falling. Since the downturn in the economy is also likely to curb demand somewhat, price pressure will abate further. In an economic environment such as this, we can well imagine the ECB making its first rate cut in less than 12 months.

We expect the bull run to continue based on the fact that, in our experience, upward-trending stock market cycles typically do not peak until we reach a high level of M&A activity and/or distinct market euphoria. There is no sign of this at the moment.

A combination of very cheap valuations in Europe in global terms, the significant discount on small caps and the fact that the end of high interest rates is in sight is conducive to equities soaring towards fresh historical highs. Investors who remain patient like us and hold very successful companies with strong growth potential and an attractive valuation will be rewarded with attractive returns.