Daniel is 26 and finished college a couple of years ago. He lives in Frankfurt am Main, in the Nordend part of town, and many people who live there like to bike to work. In the neighbourhood there are various organic supermarkets where he can buy sustainable products – sure, they cost more but at least they’re sustainable. Daniel says he is now a proud “part-time vegetarian” - one reason being his desire to reduce his personal carbon footprint. “We have to learn self-denial and to tighten our belts; our generation cannot continue to live the way others have,” he explains. “If only everybody played their part and set a good example, we could achieve a lot.”

In the beginning – 30 or 40 years ago – the community of environmentalists and climate activists in Western nations was very small.

These days, Daniel is one of many. One of a hundred thousand young people in Germany who grasp how important protecting the environment is.

Germany’s 83 million inhabitants are responsible for approximately 2.4% of global carbon emissions and make up 1% of the world’s population. However, the young people in Nordend also know that they alone cannot stop climate change - even if Germany were to cease producing all emissions from tomorrow. Nevertheless, they believe Germany should set an example and show how things could be done.

Making a show of cutting consumption not the right approach on international stage

The argument that it’s ok for the price of climate protection to be high does not wash with emerging countries. Besides, people in India and China want to drive cars, eat meat and use their air conditioners just like everyone else. Emerging countries’ response to the practice of self-denial by cutting spending and reducing wealth, which the younger generation is pushing in industrialised countries, will be, “That’s not for us. We want growth and prosperity, and we’re just as entitled to this development as the nations who’ve already reached that stage.”

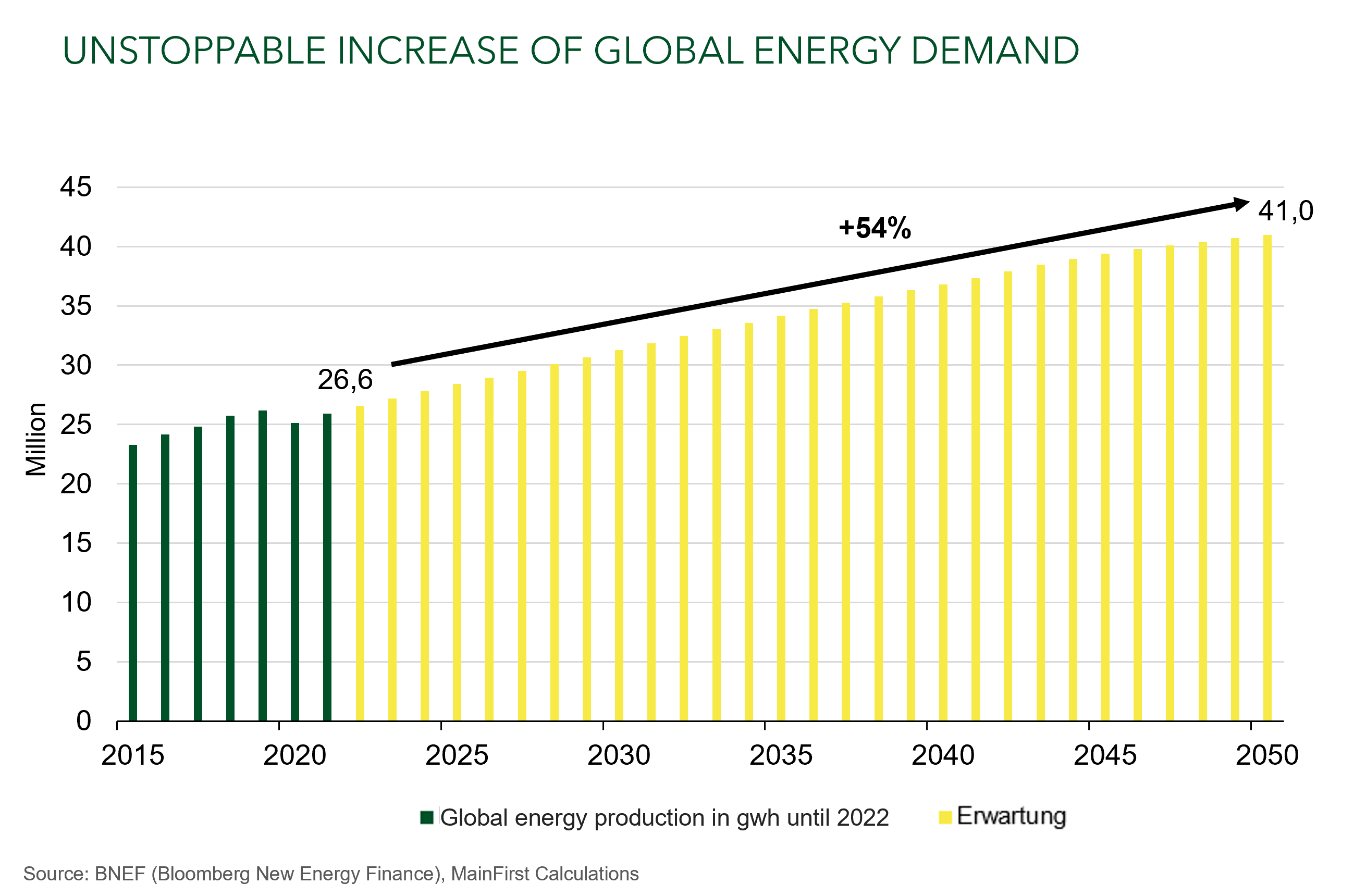

According to current calculations by BNEF, a research company that specialises in the energy market, global electricity demand will increase to approximately 41 million gigawatt hours between now and 2050 - an increase of 54% on today. This trend is undisputed in academic circles.

Our task - as a relatively small, wealthy industrialised country with a science- and technology-oriented workforce - should be to produce energy as cheaply and with as low carbon emissions as possible and to use it to enhance the standard of living. However, this model of Swabian thriftiness is unlikely to appeal to any emerging country.

Automotive industry: Germany’s biggest source of wealth in the past 70 years

The German automotive industry, the country’s biggest source of wealth in the past 70 years and which became even more globalised at the height of its maturity after the fall of the Iron Curtain in 1989, is now distinctly shaky on its feet.

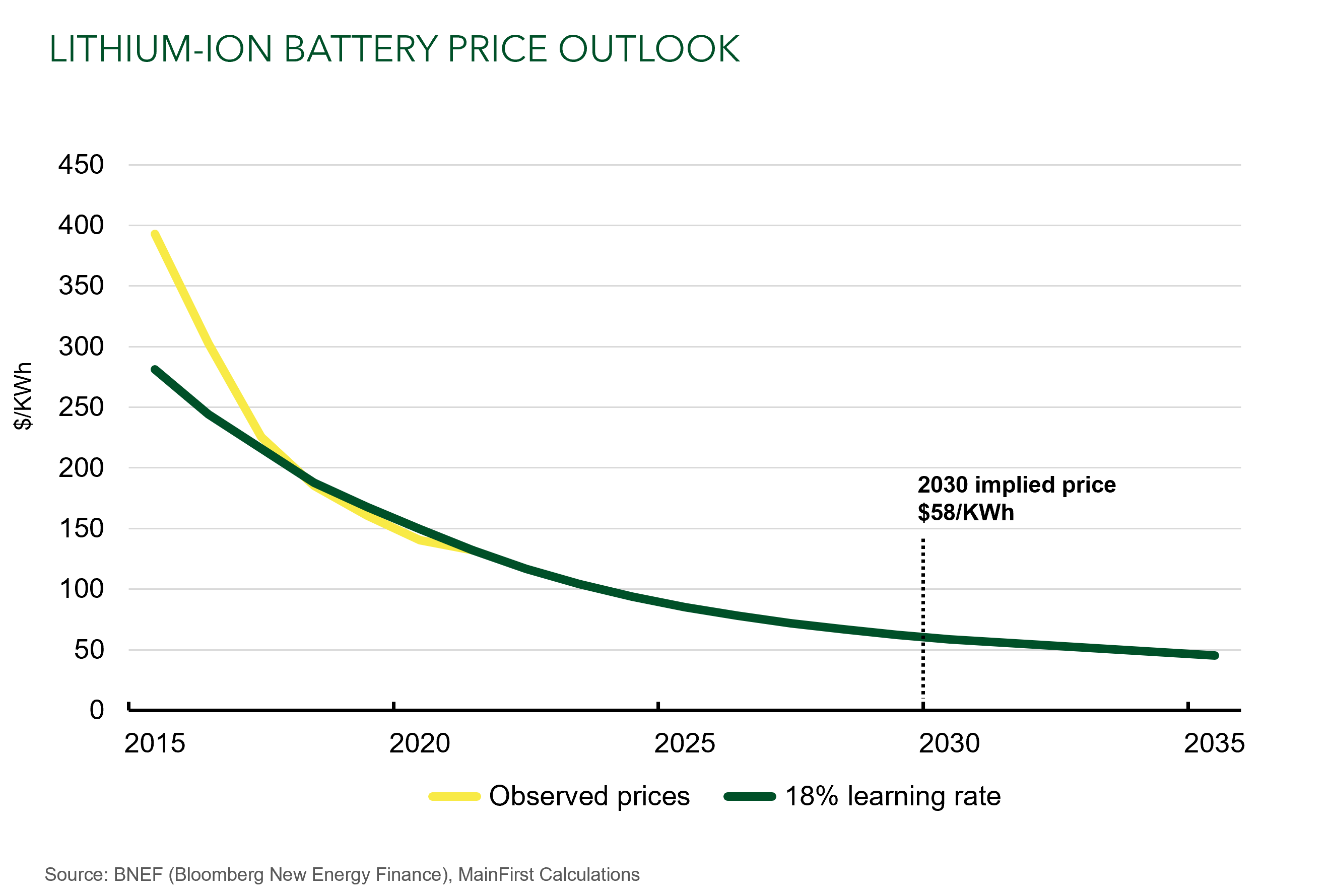

At the same time, policy and technology paved the way for battery-driven e-mobility. Cost of purchase and range have reached a tolerable level for consumers.

There were 17.4 million e-cars registered worldwide in 2021 - around six million more than in 2020 - and the trend is rising. The success of e-cars proves Elon Musk right in having committed to electric technology early and without compromise. With sales of 936,000 cars in 2021, his company is the global market leader. Despite how large Tesla has become, its growth does not seem to be slowing. Production capacity will grow to approximately 2,000,000 by year-end. Contrary to the scepticism of recent years, the company is now profitable, reporting a Q2 2022 net profit of USD 2.26 billion. Its Chinese competitor BYD, which has its origins in battery cell production, has grown to a similar size in recent years and is now producing one million fully electric cars per year, putting it in second place behind Tesla. Located in Shenzhen, China, the company only recently switched car production over to 100% electric cars - with the last combustion engine cars having come off the production line in March - and is also turning a profit.

Both companies have big plans. Musk claims Tesla will continue to grow at an average of 50% for several years. The company has set a production target of 20 million vehicles per year by the end of the decade. Such figures might sound like delusions of grandeur to some. Never before has there been car manufacturing on such a scale. However, the targets which the Texas-based company has set itself in the past have often been met with startling precision.

Its profitability is no accident. While Tesla raised its prices right across its product range by up to USD 6,000 in 2022, production costs are steadily falling thanks to greater economies of scale. When the Model 3 was launched, each car was costing USD 56,000 to manufacture. With the launch of the latest generation of “4680” batteries, which are used in the Brandenburg factory, production costs will come in under the USD 30,000 mark.

Tesla’s competitors are still far off such success stories. So-called traditional car makers’ production is not vertically integrated. In other words, they rely on dozens of suppliers at every stage of the process. This costs flexibility, speed and innovation. While VW contends with its trade unions and continues to seek talented software developers – the group as a whole still managed to sell 263,000 e-cars last year – BMW is still trying to find traction with unit sales of 104,000. The Bavarian company’s target is for sales to be 50% electric by 2030. But it has not yet gone so far as to give an absolute target for number of units.

What could the traditional manufacturers change to have a chance of competing in the future?

We already know that demand for cobalt, lithium and copper will be extremely high in the coming years. European car makers have long underestimated the importance of raw material supplies. According to an analysis by the EU Commission, we have to import more than 65% of the raw materials required for electric engine production from China.

The success of model competitors like BYD, on the other hand, is no accident. No other country dominates the mining of raw materials required for batteries as much as China.

Chinese companies were involved in nine out of ten stakeholdings in reserves of raw materials in recent years. China refines and processes 60% of all the cobalt mined in the world. The majority of the cobalt comes from the Democratic Republic of the Congo. China is involved in almost every project, either on the financial or operational side, or provides infrastructural aid. It is aware of the necessity of the raw material in the dawning age of the battery.

BYD, the second-largest producer of lithium-ion batteries for electric cars, uses 90% of its cells in its own car production, which doesn’t leave much even for competitors who are willing to pay. In June of this year, the company purchased six more lithium mines across the African continent in order to secure battery production up to 2029.

Elon Musk is also ensuring he has the capacity to realise his plans. In November 2021, Tesla concluded a three-year supply contract with Ganfeng Lithium. Under the deal, 20% of annual production will be supplied to Tesla.

The chemistry of battery cells is changing, and this is making nickel an increasingly important metal. There are significant reserves in Indonesia, for example. In August of this year, it was announced that Tesla had secured approximately one third of global nickel production under a massive five-year supply contract with several Indonesian companies. This is enough for five million cars.

As of 2021, the ten largest battery producers were in Asia - scattered around China, South Korea and Japan. They account for around 94% of global capacity, and on a rising trend.

The German car industry has long pursued a strategy of purchasing resources. Experts believed this was easier and more efficient.

Germany’s dependence is just as great when it comes to raw materials for renewable energy. The EU Commission reports that 54% of the materials for wind turbines and 53% of the resources for photovoltaic installations are imported from China.

With regard to raw materials for e-mobility and renewable electricity generation, we are wandering into exactly the same position of dependence in which we currently find ourselves in relation to Russian gas supplies. Investigative journalist Christoph Keese from publishing house ThePioneer hit the nail on the head with his article on raw material dependence.

”We want invisible prosperity. Wealth with no trace of how it came about: industry that leaves a trail of smoke is not the kind of industry we want in Europe.”

Human rights violations and inadequate environmental protection have been the hallmarks of raw material mining to date. But it doesn’t have to stay that way. The Global Battery Alliance, which advocates clean and fair production conditions, was established in Europe in 2017. The opportunities for improving African supply chains would inevitably be greater if raw material mining were managed by Europe than if the Chinese state were given free rein. Yet Europe is happy to wear its veil of innocence -at high cost.

The Taiwan risk

With a trading volume of EUR 245 billion, China was again Germany’s biggest trading partner in 2021 -and has been since 2015. Any outbreak of war between China and Taiwan, resulting in China being sanctioned to a similar extent as Russia has in the current Ukraine conflict, would be an economic disaster for Germany. By way of comparison, Russia was only Germany’s 14th biggest trading partner. Approximately 60% of Russian imports consist of oil and gas – goods that, given their nature, could hardly be more uniform or more replaceable.

Much of our prosperity is based on the expansion of our trading relations with China that has been under way since the 1990s. Four out of every ten cars that Volkswagen sells go to China. More than 90% of products that we can order on amazon.com are produced there. Consumers benefit across the board from the global division of labour. 98% of rare earths that we need in Europe for solar cells, wind turbines and batteries come from the People’s Republic. If the West imposed similar sanctions on China, all the lights would go out here. It is not “just” oil and gas that has to be sourced from elsewhere. Such a scenario would cause considerable pain on both sides. This fact makes escalation less likely, but does not rule it out. However, the passage of time is working for - rather than against - the People’s Republic of China. Every year its dependence on the West declines, the country’s tertiary sector gets stronger, and long-term raw material supplies seem largely to be secured. The relative economic power of the country continues to grow. It is now a high-tech country on which the whole world is dependent. China has set itself major targets for 2050, although that remains some time off.

Even though Daniel from Frankfurt and his generation are doing the right thing, focusing on our own borders is not enough when it comes to fighting climate change. Europe’s policy of aiming for a more sustainable economy does set intercontinental standards. Yet if we are to pass these approaches on to other continents, we need to promote, support and become part of the supply chains required for the technological achievements of the future. We don’t need to be rich - just independent.

Author: Jan-Christoph Herbst, Portfolio Manager of the MainFirst Global Equities Fund, MainFirst Global Equities Unconstrained Fund, MainFirst Megatrends Asia and MainFirst Absolute Return Multi Asset