Rising interest rates and aggressive central bank actions weighed on the fixed income market in 2022, including emerging markets (EM) corporate credit. The war in Ukraine further depressed investor sentiment and pushed commodity prices higher. Rising inflation and import prices led to the default of some weak frontier markets such as Sri Lanka, contributing to the misperception that all EMs would suffer equally from rising prices. 2022 was also the year of the slowest Chinese economic growth since the mid-1970s. Strict lockdowns and restrictions across China led to a global supply chain problem, depriving the world of its second-most-powerful economic growth engine, which is particularly important for many other export-oriented economies in the EM space. In this uncertain environment, global equities lost 18.1% last year, while US and EM credit lost 13% and 12.3% respectively. The clear winners were commodities, which benefited from scarcity and dislocation, and the USD, which benefited from the Federal Reserve’s aggressive monetary tightening.

However, now that 2022 is behind us, we believe that the current landscape is very different from three months ago and that the backdrop is now favourable for developing economies. Inflation figures have started to slow and central bankers are openly discussing the end of this hiking cycle, given the negative impact of tighter financial conditions on the real economy. This has already pushed Treasury yields lower and contributed to a weaker USD, which has benefited EM assets (investors tend to associate a strong dollar with rising refinancing problems for EM corporates and sovereigns). We don’t think this trend is over yet and expect lower Treasury yields and a weaker USD from current levels. In a further boost to sentiment, China decided in November to reverse course and re-opened its economy. This change in strategy will allow the Chinese economy to rebound in 2023, with positive spillovers for other countries, especially in the EM world. On the other hand, one of the few things that hasn’t changed from 3 months ago is that commodity prices are still at elevated levels, which is positive for many commodity exporters in the EM space. Against this backdrop, we are positive on EM corporate credit and we expect the asset class to deliver further positive returns this year, following the 10% rally since November 2022. While growth will inevitably slow down this year, the growth differential between emerging and developed markets is expected to widen in favour of the former this year. At the same time, EM companies have strong fundamentals and their valuations are not expensive.

Below, we briefly discuss our key beliefs for 2023 and why we believe they make EM corporate credit attractive both in absolute terms and relative to other fixed income asset classes.

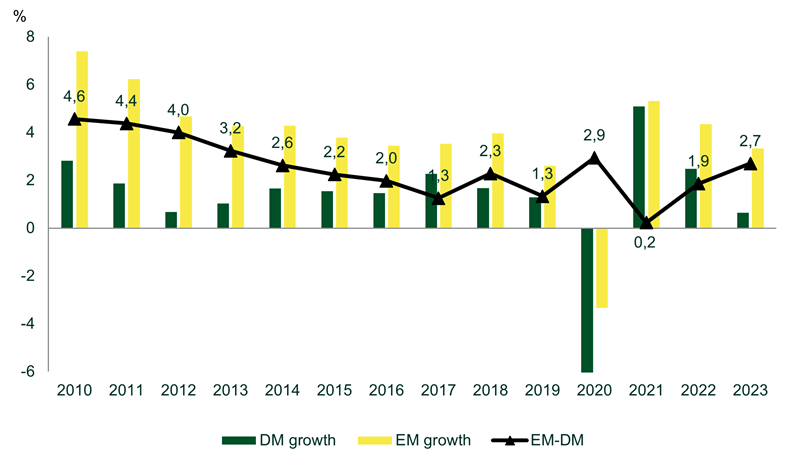

EM corporates have strong fundamentals and can weather a slowdown in economic growth this year. They are entering 2023 with historically low levels of leverage. Net leverage (net debt/EBITDA) stands at 1.1x, the lowest level since 2008. This underlines the strong ability of EM corporates to sustain their debt and avoid a massive wave of defaults in the event of a global growth slowdown. Areas of stress remain, but they are limited to the idiosyncratic stories of 2022, namely the crisis in China’s real estate sector and the war between Russia and Ukraine. To put the above figures into perspective, the net leverage of investment-grade (IG) and high-yield corporates in the EM market is currently 0.9x and 1.8x respectively. This compares with 2.5x and 3.6x for US IG and US HY and to 3.3x and 5.0x for EUR IG and HY respectively. While net leverage may increase slightly this year given the global slowdown, the increase should be limited and not exceed 0.2x/0.3x. From this perspective, some relative economic growth of developing versus developed economies should provide some support. This year, as shown in Fig 1, the growth differential between EM and DM is expected to widen in favour of the former. This is supported by the IMF’s latest growth projections.

Fig 1. Comparison of EM and DM growth rates. Growth rates are computed as the average growth rate of the 7 largest emerging countries (excl. Russia) and the average growth rate of the 7 largest developed countries. The differential is computed as the difference between these two averages.

Source: IMF, MainFirst. IMF projections.

In many DM countries, the growth outlook darkens as debt as a percentage of GDP rises sharply following the pandemic. In Japan, the gross debt/GDP increased by 27.5% over the 2019-2022 period, while in the US, Germany and Italy it increased by 12-15%. At the same time, debt has been much more stable in many emerging markets , especially in Latin America and the Middle East. Brazil and Mexico are good examples, as their gross debt/GDP increased by only 0.32% and 3.5% respectively. In the Middle East, if we take Saudi Arabia, a country that has benefited from high energy prices, this ratio has only increased by 2.3%. This suggests that it is the DM that could run into trouble in the future from a debt-sustainability perspective. Furthermore, long-term factors such as a younger and in many cases still-growing population also argue for stronger economic growth in the developing economies, where an ageing and shrinking population is a major obstacle to future growth.

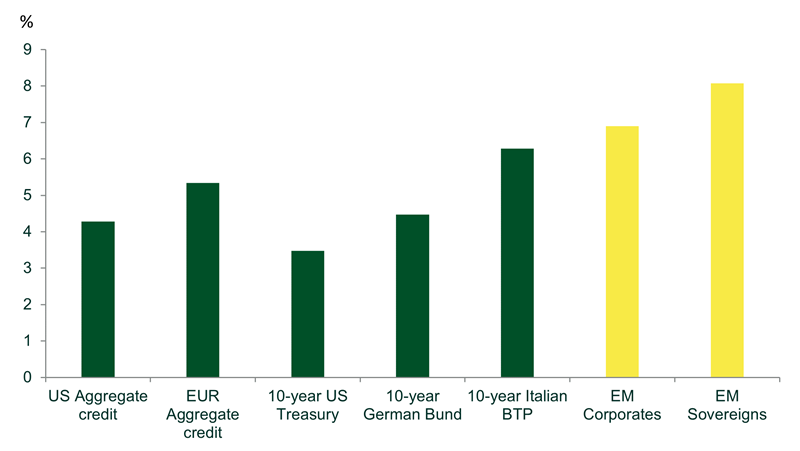

Strong fundamentals come with attractive valuations. EM corporate bonds are not expensive. Historically, when spreads for the asset class have been above current levels (321 bps), the return over the next 12 months has been around 10%. The CEMBI BD index (our benchmark) currently offers a yield-to-maturity (YTM) of 6.6%, while our fund offers a yield of 9.5% (data as of January 2023). These figures look very attractive in a context of declining but still-elevated inflation this year. Emerging market fixed income segments generally offer an attractive yield pick-up over their developed market counterparts. Fig 2 shows how emerging market segments offer a higher yield than US and EUR government and credit.

Fig 2. YTM of the main fixed income segments in USD. For EUR segments, the yield is hedged in USD

Source: Bloomberg, Mainfirst. Data as of 8 February 2023.

Emerging markets are benefiting from the commodity markets boom. Strong fundamentals and better growth rates in emerging markets have also been associated with rising commodity prices over the past 2 years. With the exception of Australia and Canada, the main commodity producers are all in emerging markets. The long-term story is linked to the fact that market fundamentals remain very supportive. Low inventory levels in the physical markets are some of the tightest in a long time, and are only getting tighter. In addition, the CAPEX cycle has yet to really kick in, pushing the production response further into the future and adding to the undersupply. While CAPEX is slightly higher YoY in 2022, the increase merely reflects inflation. In the short-term, as the Fed completes its cycle of interest rate hikes and the economic outlook improves, we will see the next rise in commodity prices, similar to the last cycle that started in 2002 or also in the 1970s. The reopening of China is also an important support for commodity prices, given that the country accounts for more than 50% of total imports of certain metals.

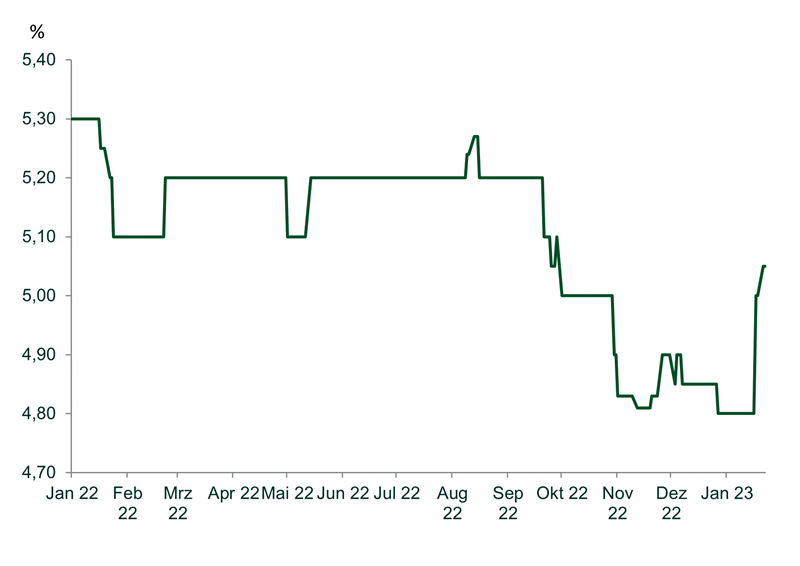

China’s reopening is a positive sentiment boost for EM. The removal of restrictions will benefit China in the first instance, but also other countries. The risk of new variants remains and is something we are continuing to monitor, but the reopening will ultimately benefit Chinese growth and allow the country to recover from the self-inflicted pain of the past year. Fig 3 shows how economists have already started to revise up their growth estimates for 2023. However, the rebound in economic growth may not be linear, as many consumers may still be reluctant to go out and behave as they would have in 2019. While much of the growth will come from rising consumer spending and services, other countries should also benefit, especially in the ASEAN region. Countries such as Thailand, for example, are highly dependent on tourism, which typically accounts for 10-12% of GDP. A large proportion of tourists in Thailand and in Southeast Asia in general come from China, so these countries will benefit from rising travel spending and improved mobility in China. Other countries, such as South Africa, should also benefit given its strong trade links with China.

Fig 3. China – Median GDP economic forecast for 2023 (YoY %)

Source: Bloomberg, Mainfirst. Data as of 8 February 2023.

Source: Bloomberg, Mainfirst. Data as of 8 February 2023.

Finally, we expect EM corporate credit to benefit from lower rates and a weaker USD. As mentioned at the beginning, while US Treasury yields and the dollar have come down from their peaks around September/November last year, we still believe that this trend is not yet over. US economic data has deteriorated over the past two months, particularly in the housing market. Going forward, we believe that the Fed will have to change its tone as the data continues to deteriorate and adjust its monetary policy accordingly. We expect this to push interest rates further down. As the data has started to deteriorate, several Fed speakers have already started to talk about slower rate hikes and peak rates. Of course, softer inflation prints are also supportive of our view. As US interest rates fall, the USD will weaken further, while more cyclical currencies will also be supported by the reopening of China and higher commodity prices. While a weaker USD will support the debt sustainability of emerging economies, especially those with a significant USD debt, it is also worth noting that many large EMs like Brazil, Mexico, Chile and Indonesia have developed well-functioning local-currency markets and pension systems over the past few years. This allows such economies to eliminate foreign currency risk and diversify their debt mix, sometimes with a more attractive alternative (lower risk premium on interest rates). One example is Brazil, where companies now borrow mainly in local currency. In other words, developing countries are less vulnerable to the USD than what many investors think.