- Marketing Communication -

Dividends are highly valued by investors and represent an essential component in the asset allocation of the overall return on equity investments. In times of low interest rates, in particular, investors look forward to attractive payouts and consequently there is a great deal of pain when, as in the pandemic year of 2020, there are reductions or even cancellations. We would like to take a look into the “dividend” treasure chest and examine not only the historical phases but also their current recovery.

In a study, UBS Bank analysed the contribution of dividends, assuming they are reinvested, to total returns in Europe. The result is impressive; according to the UBS study, dividends account for up to 60 percent of total returns over the long term. In addition, distributions offer investors an attractive payment stream in times of structurally low interest rates. Of course, the joy of dividends only exists as long as they are paid out. Based on the experience of the 2020 pandemic year, the pain of cancelled or reduced dividends still runs deep.

The oil magnate John D. Rockefeller once said that Standard Oil's regular dividend payments always gave him a great deal of pleasure. He probably wouldn't have been inspired to make this statement if his distributions had been irregular and of an uncertain amount. But how do dividend payouts behave in times of crisis and how does their recovery develop?

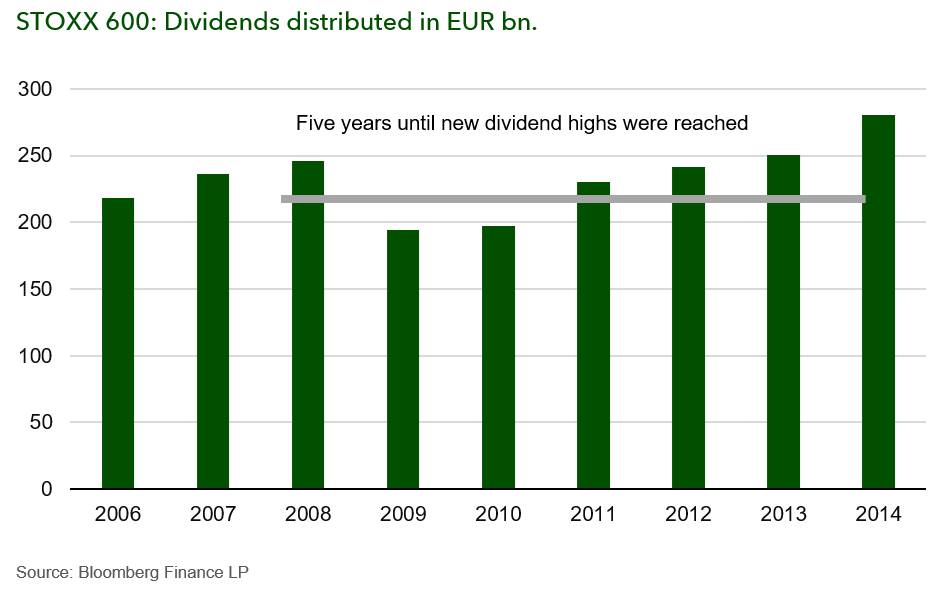

Let us first look at the onset of the global financial crisis from 2008 onwards. In 2008, the index stocks from the European STOXX 600 paid out dividends amounting to 246 billion euros. In the following year, 2009, the amount fell to 194 billion euros, a decrease of more than 20 percent in the dividend amount. Subsequently, it took a total of five years (see Graph) until new dividend highs were reached.

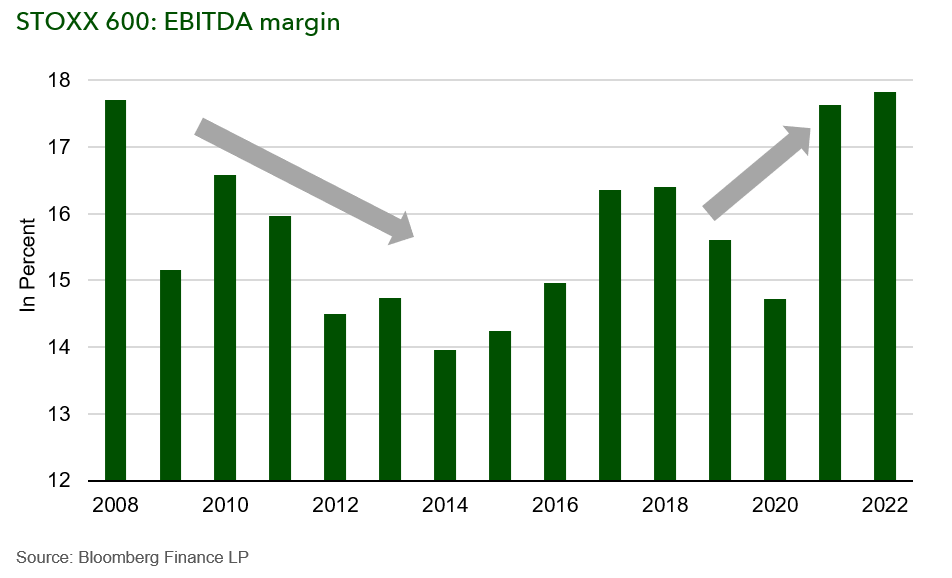

The recovery period of five years is linked to several complex aspects. Banks and commodity stocks, as well as energy stocks, which accounted for a high share of the distributions, took a long time to clean up their balance sheets or suffered from the decline in world market prices. Furthermore, companies have taken a long time to repair their balance sheets and achieve sustainably attractive (EBITDA) margins (see Graph). An additional, purely European, problem after the financial crisis was the euro crisis with the indebted peripheral states. All in all, these aspects led to a longer recovery phase.

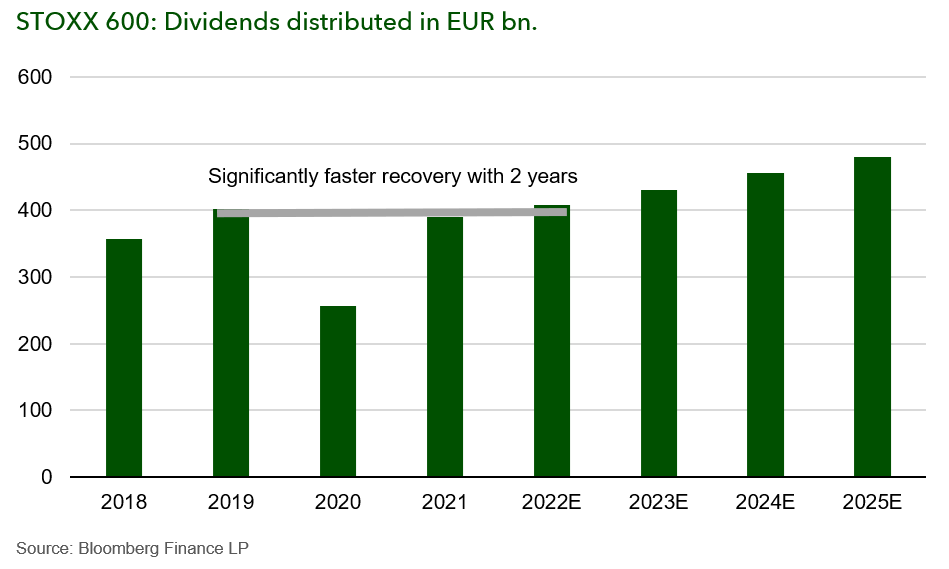

Dividend amounts, which were reduced in the wake of the pandemic, have seen a much faster recovery. In the “Annus Horribilis” of 2020, dividends of 257 billion euros were distributed, a drop of 36 percent compared to the previous year. However, we already expect new record dividend amounts for 2022 (see Graph 3), i.e. only two years after the outbreak of the pandemic. In other words, the recovery has been much faster than it was after the last global crisis in 2008. This is due to several factors. First, the framework conditions at the macroeconomic and monetary level are different. The support measures taken by individual nations across all sectors of the economy, in particular their speed and scale, have contributed significantly to the recovery. Advantageous corporate loans and short-time work (Kurzarbeit) or working from home have had an equally large impact. Furthermore, central banks have flooded the markets with almost unlimited liquidity, with the first interest rate hikes now already on the cards in the US. At the corporate level, primarily due to supply chain disruptions and unabated high consumer demand, we are seeing inflationary pressures that we have not seen in Europe for more than 30 years. The inflation rate is threatening companies’ profitability, but they have already taken countermeasures through dynamic cost adjustments and price increases (see Graph).

Due to the continuing positive macroeconomic conditions and dynamic adjustments, companies across the board will reach or even exceed the profitability levels of 2019. Based on these expectations, they are capable of reaching new highs in terms of dividend amounts. Dividend hunters should therefore not miss the chance for attractive payouts.

Authors: Christos Sitounis und Thomas Meier, Portfolio Managers for the MainFirst Global Dividend Stars & the MainFirst Euro Value Stars

DISCLAIMER

This is a marketing communication addressed exclusively to professional and/or eligible counterparties in accordance with the MiFID II Directive (2014/65/EU).

This marketing communication is for information purposes only and provides the addressee with guidance on our products, concepts and ideas. This does not form the basis for any purchase, sale, hedging, transfer or mortgaging of assets. None of the information contained herein constitutes an offer to buy or sell any financial instrument nor is it based on a consideration of the personal circumstances of the addressee. It is also not the result of an objective or independent analysis. MainFirst makes no express or implied warranty or representation as to the accuracy, completeness, suitability, or marketability of any information provided to the addressee in webinars, podcasts or newsletters. The addressee acknowledges that our products and concepts may be intended for different categories of investors. The criteria are based exclusively on the currently valid sales prospectus. This marketing communication is not intended for a specific group of addressees. Each addressee must therefore inform themselves individually and under their own responsibility about the relevant provisions of the currently valid sales documents, on the basis of which the purchase of shares is exclusively based. Neither the content provided nor our marketing communications constitute binding promises or guarantees of future results. No advisory relationship is established either by reading or listening to the content. All contents are for information purposes only and cannot replace professional and individual investment advice. The addressee has requested the newsletter, has registered for a webinar or podcast, or uses other digital marketing media on their own initiative and at their own risk. The addressee and participant accept that digital marketing formats are technically produced and made available to the participant by an external information provider that has no relationship with MainFirst. Access to and participation in digital marketing formats takes place via internet-based infrastructures. MainFirst accepts no liability for any interruptions, cancellations, disruptions, suspensions, non-fulfilment, or delays related to the provision of the digital marketing formats. The participant acknowledges and accepts that when participating in digital marketing formats, personal data can be viewed, recorded, and transmitted by the information provider. MainFirst is not liable for any breaches of data protection obligations by the information provider. Digital marketing formats may only be accessed and visited in countries in which their distribution and access is permitted by law.

For detailed information on the opportunities and risks associated with our products, please refer to the current sales prospectus. The statutory sales documents (sales prospectus, key investor information documents (KIIDs), semi-annual and annual reports), which provide detailed information on the purchase of units and the associated risks, form the sole authoritative and binding basis for the purchase of units. The aforementioned sales documents in German (as well as in unofficial translations in other languages) can be found at www.mainfirst.com and are available free of charge from the investment company MainFirst Affiliated Fund Managers S.A. and the custodian bank, as well as from the respective national paying or information agents and from the representative in Switzerland. These are:

Austria: Raiffeisen Bank International, Am Stadtpark 9, A-1030 Wien, Österreich; Belgium: ABN AMRO, Kortijksesteenweg 302, 9000 Gent, Belgium; Finland: Skandinaviska Enskilda Banken P.O. Box 630, FI-00101 Helsinki, Finland; France: Société Générale Securities Services, Société anonyme, 29 boulevard Haussmann, 75009 Paris, France; Germany: MainFirst Affiliated Fund Managers (Deutschland) GmbH, Kennedyallee 76, D-60596 Frankfurt am Main, Deutschland; Italy: Allfunds Bank Milan, Via Bocchetto, 6, 20123 Milano MI, Italy; Lichtenstein: Bendura Bank AG, Schaaner Strasse 27, 9487 Gamprin-Bendern, Lichtenstein; Luxembourg: DZ PRIVATBANK S.A., 4, rue Thomas Edison | L-1445 Strassen; Portugal: BEST - Banco Eletronico de Servico Toal S.A., Praca Marques de Pombal, 3A,3,Lisbon; Spain: Societe Generale Sucursal en Espana, Calle Cardenal Marcelo Spinola 8. 4t planta. 28016 Madrid, Spain; Sweden: MFEX Mutual Funds Exchange AB, Grev Turegatan 19, Box 5378, SE-102 49, Stockholm, Sweden; Switzerland: UBS Fund Management AG, Aeschenplatz 6, 4052 Basel, Switzerland; UK: Société Générale Securities Services, Société Anonyme (UK Branch), 5 Devonshire Square, Cutlers Gardens, London EC2M 4TL, United Kingdom

The investment company may terminate existing distribution agreements with third parties or withdraw distribution licences for strategic or statutory reasons, subject to compliance with any deadlines. Investors can obtain information about their rights from the website www.mainfirst.com and from the sales prospectus. The information is available in both German and English, as well as in other languages in individual cases. Explicit reference is made to the detailed risk descriptions in the sales prospectus.

This publication is subject to copyright, trademark and intellectual property rights. Any reproduction, distribution, provision for downloading or online accessibility, inclusion in other websites, or publication in whole or in part, in modified or unmodified form, is only permitted with the prior written consent of MainFirst.

Copyright © 2022 MainFirst Group (consisting of companies belonging to MainFirst Holding AG, herin „MainFirst“). All rights reserved.