For decades, globalisation has shaped world trade, politics and financial markets. Free global trade was seen as a source of prosperity. However, the dark side of the division of labour and the associated dependencies on a global scale have become apparent. Now, new geopolitical constellations, shifting priorities among major powers and a growing focus on national interests point to a world in transition. Does this mean the end of the globalists?

New US policy: Tariffs instead of taxes

With the new US administration in office, there has been a marked change in policy, with the focus shifting from international free trade agreements to revenue from import tariffs. The policy goal is to strengthen the national budget without raising domestic taxes. Ideally, income taxes would even be reduced in exchange for tariff revenues. At the same time, the aim is to protect domestic industry and improve the trade balance.

The US is thus returning to a trade policy strongly reminiscent of earlier protectionist approaches. Import tariffs are no longer used solely as a political lever, but are being established as a permanent pillar of government financing. This has far-reaching consequences: supply chains change, imports become more expensive and domestic suppliers become more competitive - at least in the short term.

In this geopolitically tense environment, international umbrella organisations are losing their relevance. The new US administration is increasingly questioning the value of international organisations such as NATO, the WHO and the WTO. Their role is being downgraded as national interests come to the fore. Confidence in multilateral institutions is declining not only in the US but also in other parts of the world. As a result, governments are taking more responsibility for their own actions. Security partnerships and health strategies may be formed on an ad hoc basis, depending on national interests.

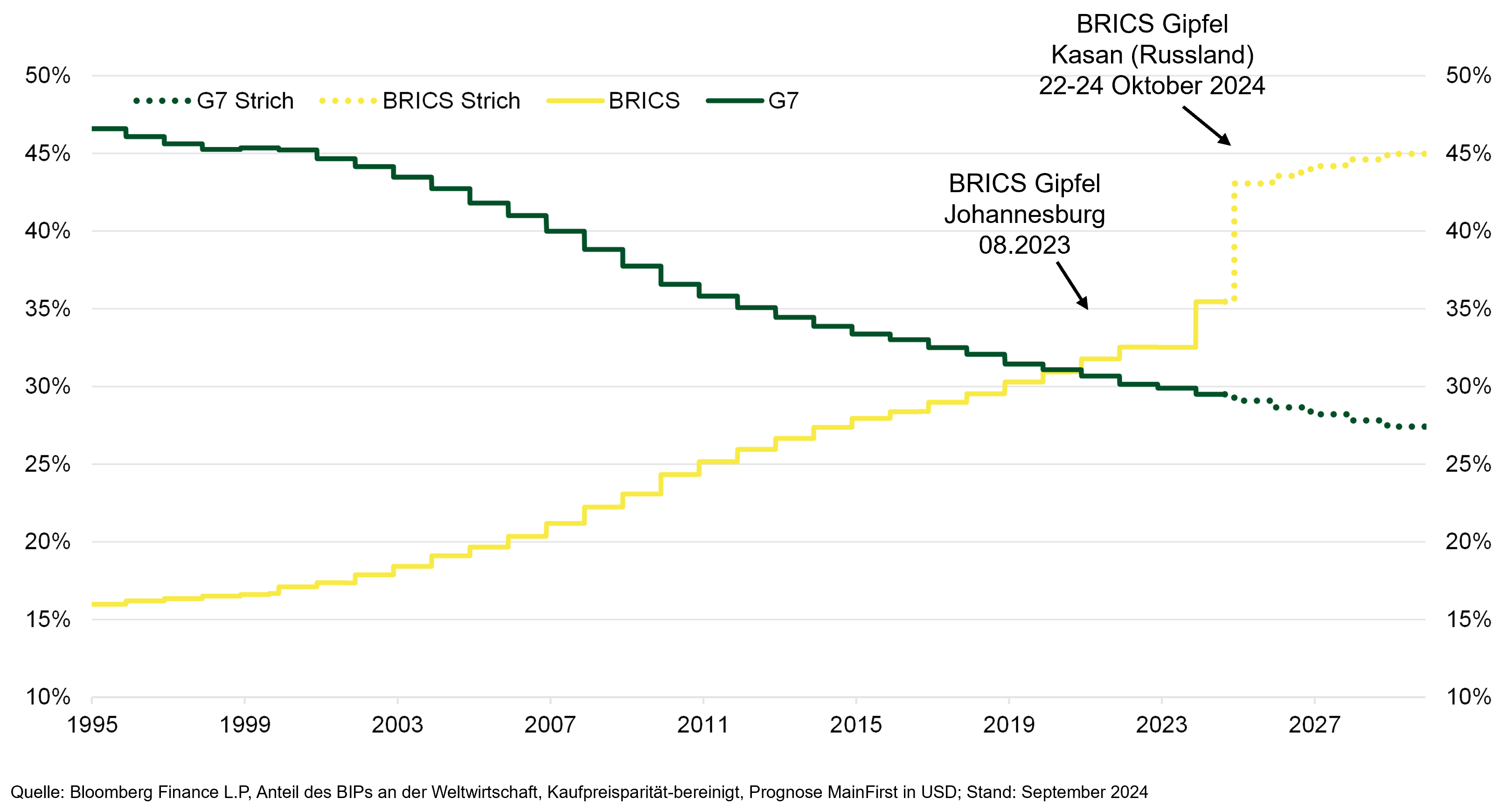

BRICS expansion: independence from the US

At the same time, many countries are increasingly seeking to diversify away from their economic dependence on the US. The BRICS alliance - originally comprising Brazil, Russia, India, China and South Africa - is expanding. More countries are showing interest in joining, including resource-rich nations such as Saudi Arabia, Argentina and Egypt. Most recently, nine new partner countries were announced at a meeting in the Russian city of Kazan in October 2024. The new partners are characterised by young and growing populations.

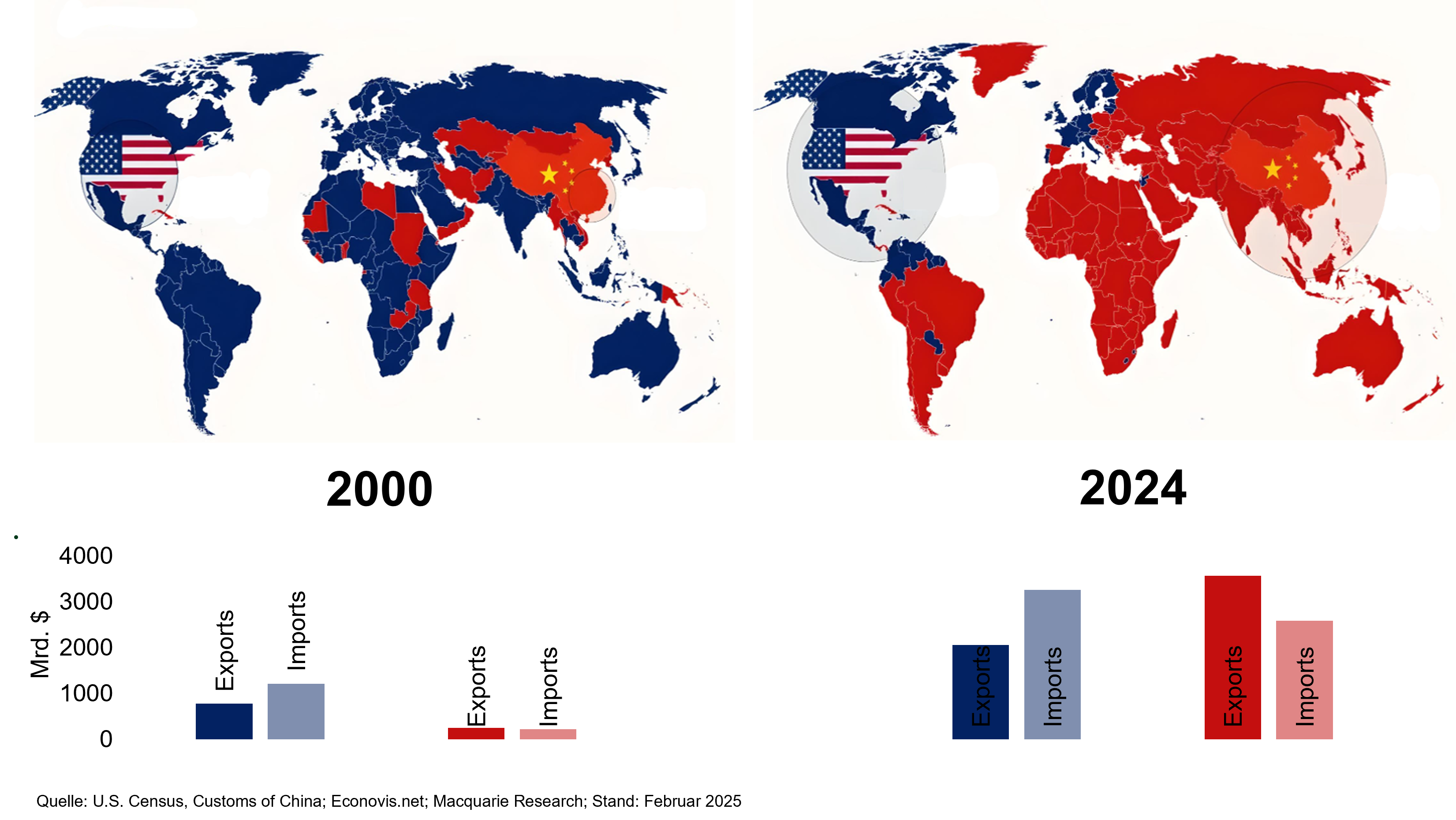

Bipolar world: USA vs. China

Despite all efforts towards multilateralism, there are many signs pointing to an accelerated development: the world is becoming increasingly bipolar, led by the two economic powers, the US and China. While the US seeks to secure its trade power through tariffs and political alliances, China is expanding its sphere of influence through investment, infrastructure projects (such as the 'New Silk Road') and targeted technology promotion.

This bipolarity creates tensions, but also new dynamics: countries are increasingly forced to take sides - either economically closer to Washington or closer to Beijing. It is becoming increasingly difficult to be in the middle. In February this year, for example, Panama officially announced its withdrawal from the Belt and Road Initiative (New Silk Road). China's strategic interest in the Panama Canal was probably a thorn in the side of the United States.

Less government spending, more entrepreneurial freedom

Another key element of the new US policy is to reduce government spending. Tax cuts, deregulation and the withdrawal of government from the economy are designed to increase entrepreneurial freedom. The focus is on innovation, personal responsibility and market dynamics.

This philosophy could spread to other Western countries. Particularly in Europe, where many economies have high public spending ratios, there is growing pressure to create more flexible and competitive conditions in order to remain competitive in the global marketplace.

The EU has become even more committed to the ideal of value-based globalisation, while other major powers have long since turned to pursuing their own hard-nosed interests.

One example is the EU's Supply Chain Act (Corporate Sustainability Due Diligence Directive, or CSDDD), which requires companies to respect human rights and environmental standards throughout their supply chains.

In the context of the trend towards national interests, less globalism and more corporate freedom (as described in the text), the Supply Chain Act runs counter to the current trend towards economic self-responsibility.

- More red tape instead of entrepreneurial freedom:

The law is forcing companies to comply with more regulations, when the global trend is actually towards deregulation and entrepreneurial responsibility. Compared to the United States, which wants to reduce its public spending, the EU is putting more restrictions on businesses. - Competitive disadvantage in a global environment:

In a world where countries such as the US and China are increasingly focusing on their own economic interests and protecting their companies, additional requirements could cause European companies to fall behind internationally.

On the other hand, individual EU countries could try to implement the law flexibly at national level or create special rules to protect their companies - which would confirm the trend towards a return to national interests within the EU.

In addition, the EU wants to expand its CO₂ certificate trading system and introduce new rules (Carbon Border Adjustment Mechanism, CBAM) designed to make imports from countries with lower environmental standards more expensive.

- Protecting industry, but risking global tensions:

On the one hand, CBAM fits well into the picture of a world in which countries are once again protecting their industries: those who import from countries with lax climate targets pay extra. The idea is to defend European standards - a kind of "green protectionism". - Risk of new trade conflicts:

However, this mechanism could lead to new trade disputes, especially with the US, China or the BRICS countries, which could see such levies as "hidden tariffs".

As a result, a trend can be observed within the European Union: national interests are regaining importance. Member states such as Poland and Hungary, but increasingly also the Netherlands and Italy, are pushing for greater autonomy in certain policy areas.

Issues such as migration policy, energy supply and trade policy are once again being discussed and decided at national level. The EU as an institution must respond by offering more flexible integration models to prevent further departures following the example of Brexit.

A stronger Europe of nations could emerge - not necessarily in opposition to the EU, but in a new, looser or smaller form of cooperation.

Impact on financial markets

These tectonic shifts have not left financial markets unscathed:

- Currency volatility: Alternative currency systems could become more important, although it would take a long time to establish them. The US dollar and other so-called fiat currencies will become pawns in geopolitical conflicts.

- Precious metals: Gain new appeal amid rising currency volatility and potential inflationary pressures. Gold and silver have been used as a store of value for thousands of years. Particularly during periods of higher tariffs, such as under President Hoover around 1930, gold was used to secure government finances. This even led to a ban on private ownership of gold. It is therefore likely that central banks will continue to buy gold as a foreign exchange reserve.

- Commodity markets: Commodities such as oil and gas will be traded more within new trading blocs. Countries such as Russia and Saudi Arabia may establish their own pricing mechanisms. We are likely to see greater stockpiling of critical commodities to minimise exposure to supply disruptions.

- Equity markets: Companies with strong international exposure will have to adjust to new tariffs, trade barriers and geopolitical uncertainties. Local champions, on the other hand, could benefit. A balanced regional allocation in a global equity portfolio is likely to be beneficial in this environment.

- Bond markets: Similar to currency markets, government bonds are likely to be used much more as a geopolitical tool in the future. It is no coincidence that the US government wants to reduce its dependence on Asian investors for refinancing US Treasuries. The focus should therefore be on appropriate interest rate sensitivity and solid credit ratings.

The signs of change are clear. The earlier vision of a fully globalised world governed by multilateral organisations is losing its appeal. Instead, national interests, economic independence and new power blocs are coming to the fore.

Whether this marks the end of the globalists or just one stage in a more complex realignment remains to be seen. What is clear is that companies, governments and investors need to prepare for a more volatile, less predictable world - with new risks, but also new opportunities.