- Marketing Communication -

It is often said that data is the new fuel for the economy. Consequently, it is not just since the pandemic that companies with data-based business models have taken a leading role in the capital markets, as demonstrated by Google or Facebook, for example. These so-called platforms use data for personalised advertising or dynamic pricing and thereby increase their profits. In order to do this, as much data as possible is collected on a global level and analysed in the cloud. Pioneers such as Amazon recognised the value of the data cloud early on and later offered this to third parties as a cloud service under the name AWS. As a result, platform companies are investing heavily in the expansion of data centres. Tencent, for example, recently announced an expansion of its cloud infrastructure with new data centres in Frankfurt, Bangkok and Tokyo, among others. This will expand Tencent's network to 27 regions worldwide. Therefore, there is a good reason why the leaders of the G7 countries recently agreed on a change in taxation, as due to increasing global networking, where companies are headquartered is becoming less important for their success.

On the other hand, we see the necessity of digitalisation for success in global competition. This has been accelerated by the coronavirus pandemic in the sense that internet data traffic has increased by almost 50% worldwide in the past year alone.

Accordingly, the digitalisation of business processes is being demanded and investments in cloud infrastructure are being driven forward. This trend has been progressing for many years and enables investors to benefit from disproportionate growth. But which company should investors back and which technology is threatened by the shift of IT infrastructure to the cloud?

Cloud infrastructure

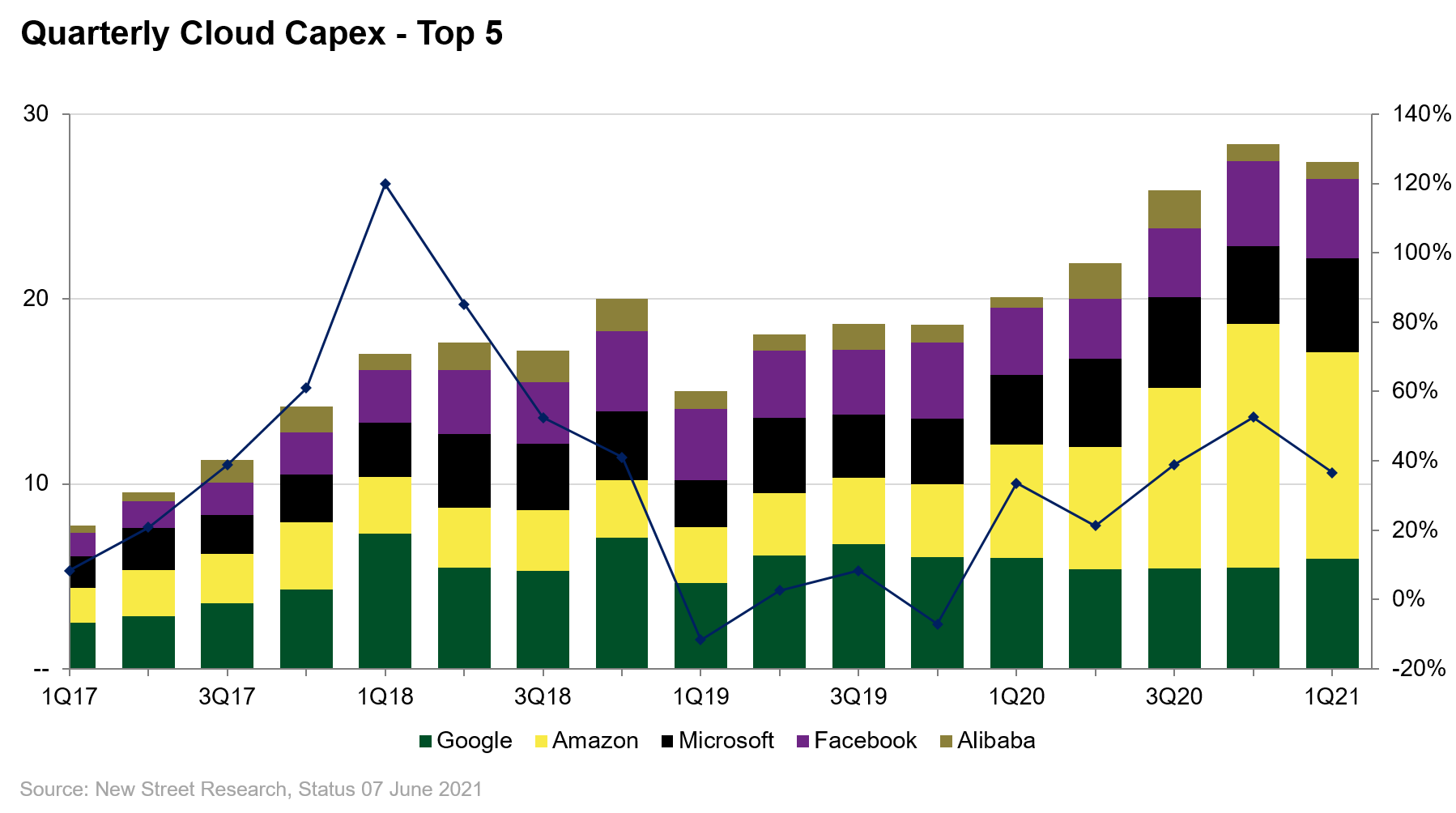

During the coronavirus pandemic, the advantages of cloud-based data storage became a critical requirement for many companies in order to maintain day-to-day operations. The extremely flexible scalability of additional storage options formed the basis for coping with the massive increase in IT usage during times of home office and video conferencing. The short-term increase in stationary server capacity would not have been possible during the lockdown phase anyway. The growth in data volumes and the demand for storage capacity in the public cloud is clearly reflected in the investments in new hyperscale data centres. In 2020, these grew by 37% alone. This means that the so-called ‘Big 7’ of the public cloud market reached over USD 100 billion in revenue in the year of the coronavirus crisis.

For investors, participation in this structural growth trend is possible with an investment in the shares of the cloud providers. However, it is important to differentiate here, as the growth in demand has not boosted all providers equally. Although larger customers increasingly prefer multi-cloud solutions so they do not risk a complete infrastructure failure in the event of a malfunction, the larger players seem to be gaining some market share.

In order to become independent of the respective cloud providers and still participate in the growth trend, investments in the hardware suppliers of data centres could also be an option. This indirect path can also be considered given that the hyperscalers operate other business activities in addition to cloud services, which can sometimes have a greater influence on the share price development. Investments in the hardware of the data centres, on the other hand, show a long-term growth trend with the volume of data.

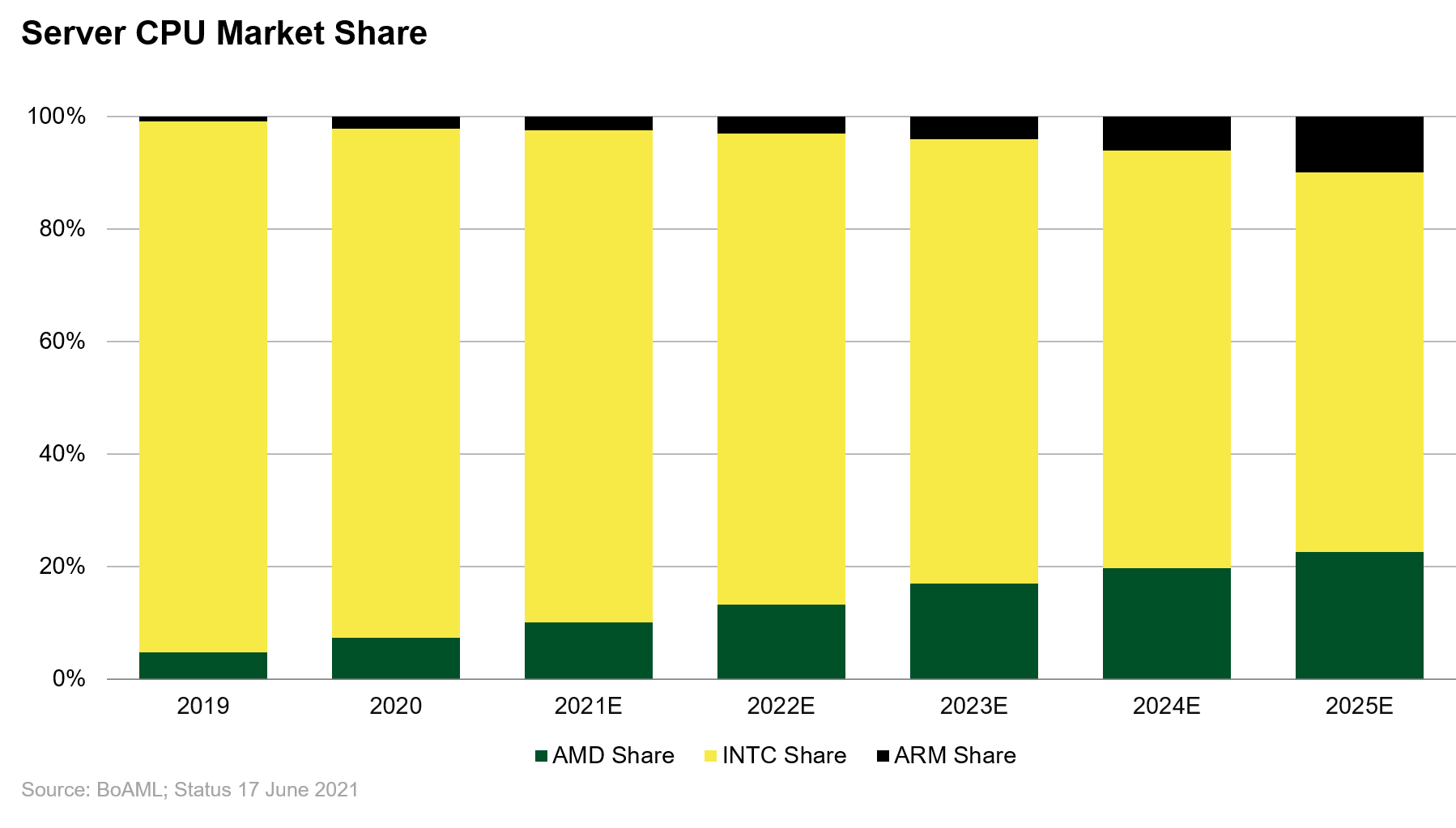

This benefits companies such as Intel, AMD or Nvidia, which provide the processors to process the data efficiently. Companies like Alphawave IP, Cadence, or Rambus, which offer products for the connectivity of data storage, also benefit. However, the performance of processors, which for many decades doubled approximately every 18 months according to Moore's Law, seems to have reached its limits. As a result, the usual server architecture with X86 microprocessors is currently being called into question. So-called GPUs (Graphic Processor Units) are increasingly being used for data processing. Or the processor architecture of ARM plc., which has already established itself as a particularly energy-efficient variant for mobile end devices, is also being brought into play for data servers. Therefore, in the area of microprocessors, market share development must also be considered and, in the case of the market leader Intel, must currently be critically assessed.

Software applications in the cloud

Typically, the general question of suitable data storage is differentiated according to the degree of self-managed components of the IT infrastructure. A distinction can be made between so-called "on premise" solutions, which are managed completely independently, through to IaaS (Infrastructure as a Service), PaaS (Platform as a Service), and SaaS (Software as a Service) solutions, which are completely outsourced. For the IT colleagues in companies, the degree of outsourcing increases the comfort in terms of maintenance and scalability of the respective services. Consequently, business models with a strong focus on service around the stationary IT system in "on premise" mode have been under pressure for years and will probably remain so.

It is a well-known fact that the relocation of IT infrastructure to the cloud takes place at different speeds depending on the complexity of the business model and other aspects such as the legal framework conditions. However, the additional offer of software applications in the cloud that can structure and evaluate existing data as quickly as possible, in addition to the usual arguments such as flexibility or reduction in IT costs, leads to an acceleration in the adaptation of cloud solutions.

A stationary system should always be designed for maximum peak load to accommodate all processes in an organisation. However, this is not economical, as many IT hardware resources would be underutilised in normal operation. With the quasi-endless scalability and the analysis tools offered, complex computing operations are made possible in the cloud, and are also easy on the IT budget.

With the relocation of data from stationary servers to the cloud, the market power of companies like IBM or Oracle is moving to AWS (Amazon Web Services), Google or Microsoft Azure. As many companies are only gradually moving their IT structure to the cloud, so-called hybrid models, i.e. a combination of stationary and cloud-based data storage, are common. For the management of the application level, a container orchestration, the so-called Kubernetes, is usually used. As this application is available as an open source system, investors can only profit from the growing data volumes to a limited extent.

In the meantime, however, larger users find that even the combination of diverse cloud providers does not pose any significant problems for integration. This makes the customers of cloud services less dependent on a cloud network and may even enable them to negotiate better prices. Multi-cloud software solutions, with which data can be managed across different clouds, are now offered in scaled-down versions free of charge. One example is Rancher, a software from Suse, a German company that recently went public.

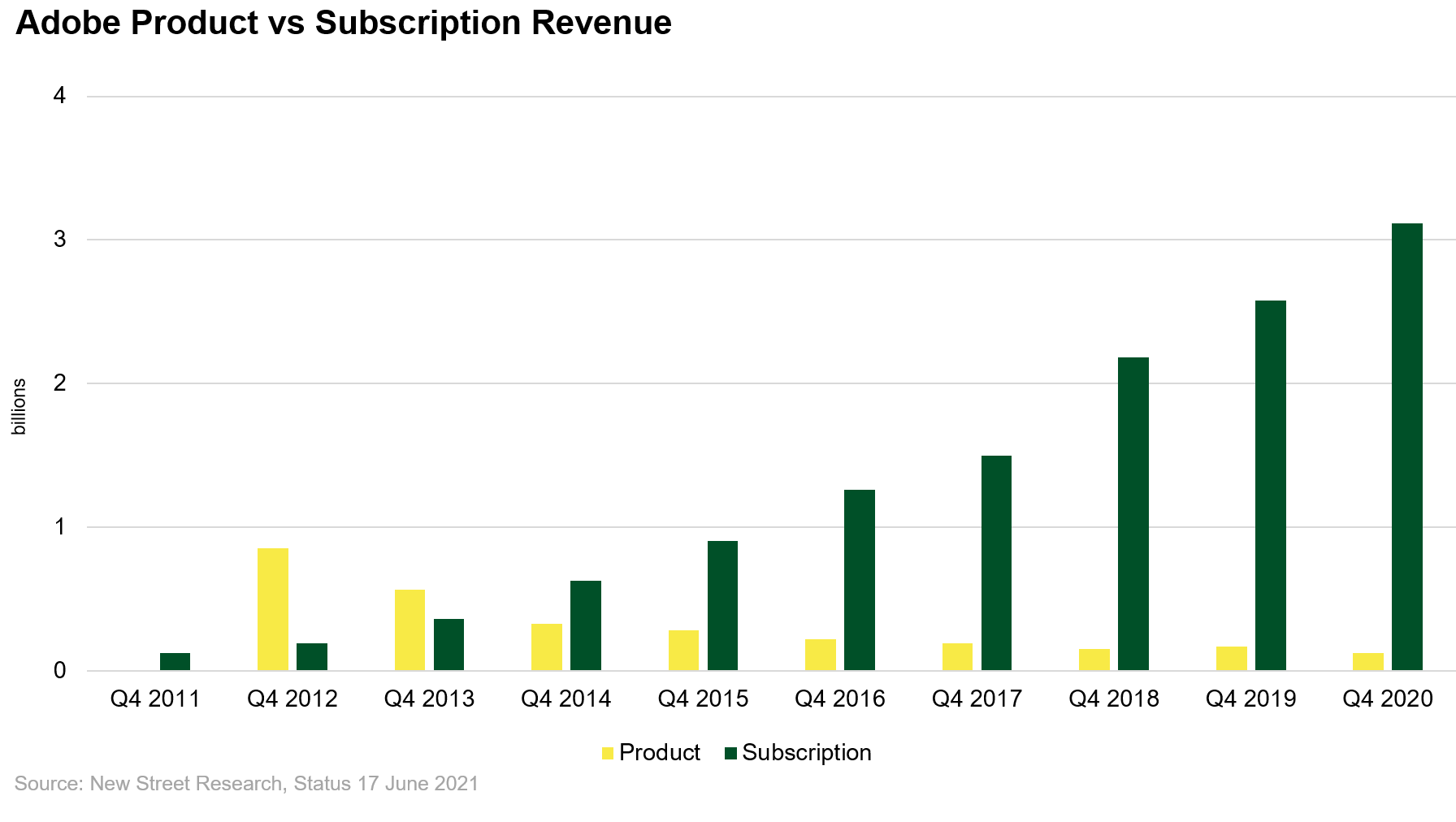

Conversely, high margins can be achieved with special software applications for the evaluation or analysis of data. Examples of this are Salesforce in the area of managing customer-specific data in sales or Adobe in the area of advertising or marketing applications. Even though the use of this software does not require an expensive licence when installed, these companies are highly valued by investors. This is because these business models are characterised by a high proportion of recurring revenues and therefore not only have high visibility but also appeal to a larger circle of users.

Leading cloud operators see the advantages of additional applications for data analysis to strengthen their customer loyalty. It is therefore not surprising that companies such as AWS, Google, and Microsoft are working very intensively on the most efficient data analysis methods possible. For cloud customers, this in turn enables better options for evaluating their own data without having to hire a large number of expensive IT specialists. A win-win situation for all involved.

As a result, several growth drivers are emerging simultaneously for various software applications. The growth of data volumes, the relocation of data to a cloud-based solution, and the growing number of IT users in light of the increasing digitalisation of society. With the typical economies of scale, margins generally increase for software developers as revenue grows. During a period of economic growth, more employees are also likely to be hired, which in turn requires more software subscriptions.

In conclusion, the advancing level of digitisation in society, the positive economies of scale on the cost side of decentralised data storage, and the increasing importance of data for business success should ensure double-digit growth in data storage in the cloud for many years to come. This is accompanied by disproportionate opportunities for investors which, as outlined above, can be capitalised on across various sub-sectors. However, the change processes here are also fast-moving and therefore require active selection.

Author: Adrian Daniel, Portfolio Manager for the MainFirst Absolute Return Multi Asset, the MainFirst Global Equities Fund & the MainFirst Global Equities Unconstrained Fund

DISCLAIMER

This is a marketing communication addressed exclusively to professional and/or eligible counterparties in accordance with the MiFID II Directive (2014/65/EU).

This marketing communication is for information purposes only and provides the addressee with guidance on our products, concepts and ideas. This does not form the basis for any purchase, sale, hedging, transfer or mortgaging of assets. None of the information contained herein constitutes an offer to buy or sell any financial instrument nor is it based on a consideration of the personal circumstances of the addressee. It is also not the result of an objective or independent analysis. MainFirst makes no express or implied warranty or representation as to the accuracy, completeness, suitability, or marketability of any information provided to the addressee in webinars, podcasts or newsletters. The addressee acknowledges that our products and concepts may be intended for different categories of investors. The criteria are based exclusively on the currently valid sales prospectus. This marketing communication is not intended for a specific group of addressees. Each addressee must therefore inform themselves individually and under their own responsibility about the relevant provisions of the currently valid sales documents, on the basis of which the purchase of shares is exclusively based. Neither the content provided nor our marketing communications constitute binding promises or guarantees of future results. No advisory relationship is established either by reading or listening to the content. All contents are for information purposes only and cannot replace professional and individual investment advice. The addressee has requested the newsletter, has registered for a webinar or podcast, or uses other digital marketing media on their own initiative and at their own risk. The addressee and participant accept that digital marketing formats are technically produced and made available to the participant by an external information provider that has no relationship with MainFirst. Access to and participation in digital marketing formats takes place via internet-based infrastructures. MainFirst accepts no liability for any interruptions, cancellations, disruptions, suspensions, non-fulfilment, or delays related to the provision of the digital marketing formats. The participant acknowledges and accepts that when participating in digital marketing formats, personal data can be viewed, recorded, and transmitted by the information provider. MainFirst is not liable for any breaches of data protection obligations by the information provider. Digital marketing formats may only be accessed and visited in countries in which their distribution and access is permitted by law.

For detailed information on the opportunities and risks associated with our products, please refer to the current sales prospectus. The statutory sales documents (sales prospectus, key investor information documents (KIIDs), semi-annual and annual reports), which provide detailed information on the purchase of units and the associated risks, form the sole authoritative and binding basis for the purchase of units. The aforementioned sales documents in German (as well as in unofficial translations in other languages) can be found at www.mainfirst.com and are available free of charge from the investment company MainFirst Affiliated Fund Managers S.A. and the custodian bank, as well as from the respective national paying or information agents and from the representative in Switzerland. These are:

Austria: Raiffeisen Bank International, Am Stadtpark 9, A-1030 Wien, Österreich; Belgium: ABN AMRO, Kortijksesteenweg 302, 9000 Gent, Belgium; Finland: Skandinaviska Enskilda Banken P.O. Box 630, FI-00101 Helsinki, Finland; France: Société Générale Securities Services, Société anonyme, 29 boulevard Haussmann, 75009 Paris, France; Germany: MainFirst Affiliated Fund Managers (Deutschland) GmbH, Kennedyallee 76, D-60596 Frankfurt am Main, Deutschland; Italy: Allfunds Bank Milan, Via Bocchetto, 6, 20123 Milano MI, Italy; Lichtenstein: Bendura Bank AG, Schaaner Strasse 27, 9487 Gamprin-Bendern, Lichtenstein; Luxembourg: DZ PRIVATBANK S.A., 4, rue Thomas Edison | L-1445 Strassen; Portugal: BEST - Banco Eletronico de Servico Toal S.A., Praca Marques de Pombal, 3A,3,Lisbon; Spain: Societe Generale Sucursal en Espana, Calle Cardenal Marcelo Spinola 8. 4t planta. 28016 Madrid, Spain; Sweden: MFEX Mutual Funds Exchange AB, Grev Turegatan 19, Box 5378, SE-102 49, Stockholm, Sweden; Switzerland: UBS Fund Management AG, Aeschenplatz 6, 4052 Basel, Switzerland; UK: Société Générale Securities Services, Société Anonyme (UK Branch), 5 Devonshire Square, Cutlers Gardens, London EC2M 4TL, United Kingdom

The investment company may terminate existing distribution agreements with third parties or withdraw distribution licences for strategic or statutory reasons, subject to compliance with any deadlines. Investors can obtain information about their rights from the website www.mainfirst.com and from the sales prospectus. The information is available in both German and English, as well as in other languages in individual cases. Explicit reference is made to the detailed risk descriptions in the sales prospectus.

This publication is subject to copyright, trademark and intellectual property rights. Any reproduction, distribution, provision for downloading or online accessibility, inclusion in other websites, or publication in whole or in part, in modified or unmodified form, is only permitted with the prior written consent of MainFirst.

Copyright © 2021 MainFirst Group (consisting of companies belonging to MainFirst Holding AG, herin „MainFirst“). All rights reserved.